If you’re a startup founder, the phrase “interest-free funding” probably sounds like a myth. Yet, a powerful, and often overlooked, financial strategy exists that provides exactly that: 0% business credit lines. Unlike traditional bank loans that come with immediate interest and strict collateral requirements, these lines offer a crucial grace period—typically 6 to 18 months—where you can use capital for growth without paying a dime in interest. This makes them a high-ROI funding vehicle for new and growing businesses.

In this comprehensive guide for 2025, we’ll demystify this powerful strategy. We’ll show you exactly how 0% business credit lines work, outline the tactical steps to qualify for large unsecured amounts, and reveal how founders are using this method to bootstrap their ventures without giving up equity. Whether you’re launching a new business or scaling an existing one, mastering this strategy could be the key to your financial freedom. Want to jump straight to the experts? Jump to our recommended 0% credit partners.

Access 0% Business Credit Lines with Fund & Grow

Unlock significant 0% interest business credit lines, ranging from $50,000 to $250,000, for your startup or growing business. Fund & Grow specializes in optimizing your credit profile to secure maximum approvals for operational and growth expenses.

- ✅ $50,000 – $250,000 in Credit Lines

- ✅ 0% Interest for 6-18 Months

- ✅ Boost Your Business Credit Score

- ✅ Expert Guidance & Support

- ✅ Ideal for Startups & Small Businesses

Learn how to leverage this powerful funding strategy for your venture.

What Are 0% Business Credit Lines & How Do They Work?

A 0% business credit line is a form of revolving credit, often issued by major banks and credit unions, that offers a promotional period with a zero percent annual percentage rate (APR). This promotional period can last anywhere from 6 to 18 months, during which time you can draw funds as needed, repay them, and reuse the credit limit without incurring any interest charges. This is distinct from a traditional business line of credit, which typically has a standard variable interest rate from day one.

The key to this strategy is that these lines of credit are often offered by a variety of issuers, allowing savvy entrepreneurs to “stack” multiple lines. By securing several of these offers, a startup can accumulate a significant pool of unsecured capital—often ranging from $50,000 to over $250,000—that can be used for a variety of business needs, from covering operational expenses to investing in marketing or inventory. This is a common tactic for founders who want to avoid the high cost of venture debt or the dilution of equity that comes with traditional investment. This strategy works particularly well for startups with limited operating history, as the approval is heavily weighted on the personal credit profile of the founder, rather than the business’s financials. For a more detailed comparison of different funding types, see our guide on Business Loans vs. Business Credit Cards.

Eligibility: What Do Lenders Look For?

When you apply for a 0% business credit line, lenders primarily assess two things: your personal creditworthiness and your business’s legal structure. Unlike a typical SBA loan which requires extensive business financials and collateral, these offers hinge on your personal FICO score.

- Personal Credit Score: A FICO score of 680 or higher is a common starting point, with scores above 720 significantly increasing your chances of approval for higher limits and more favorable terms. Lenders want to see a history of responsible credit management.

- Credit Utilization: Lenders prefer to see low credit utilization on your personal accounts—ideally below 30%, and even better if it’s below 10%. This shows you aren’t overextended and can manage new credit responsibly.

- Payment History: A clean payment history with no recent late payments is paramount. Any defaults or collections can immediately disqualify you.

- Business Structure: Having a formal business entity like an LLC or a Corporation (S-Corp or C-Corp) is often a requirement. This demonstrates a legitimate, separate entity from your personal finances. For a deep dive, check out our guide on LLC vs. S-Corp vs. C-Corp for Startup Funding.

- Annual Revenue: While not the primary factor for new businesses, some lenders may ask for proof of revenue if you’re an existing business. This is where a clean, professional bookkeeping system from a partner like Bench.co can make a huge difference.

The beauty of this strategy is that it allows a new business to access significant capital without a proven track record. The credit is granted based on the founder’s personal credit strength, making it an ideal tool for bootstrapping. However, once approved, it’s crucial to use the credit line to build a solid business credit history, which is a separate entity from your personal score. For more on this, read our comprehensive guide on Building Business Credit for Startups.

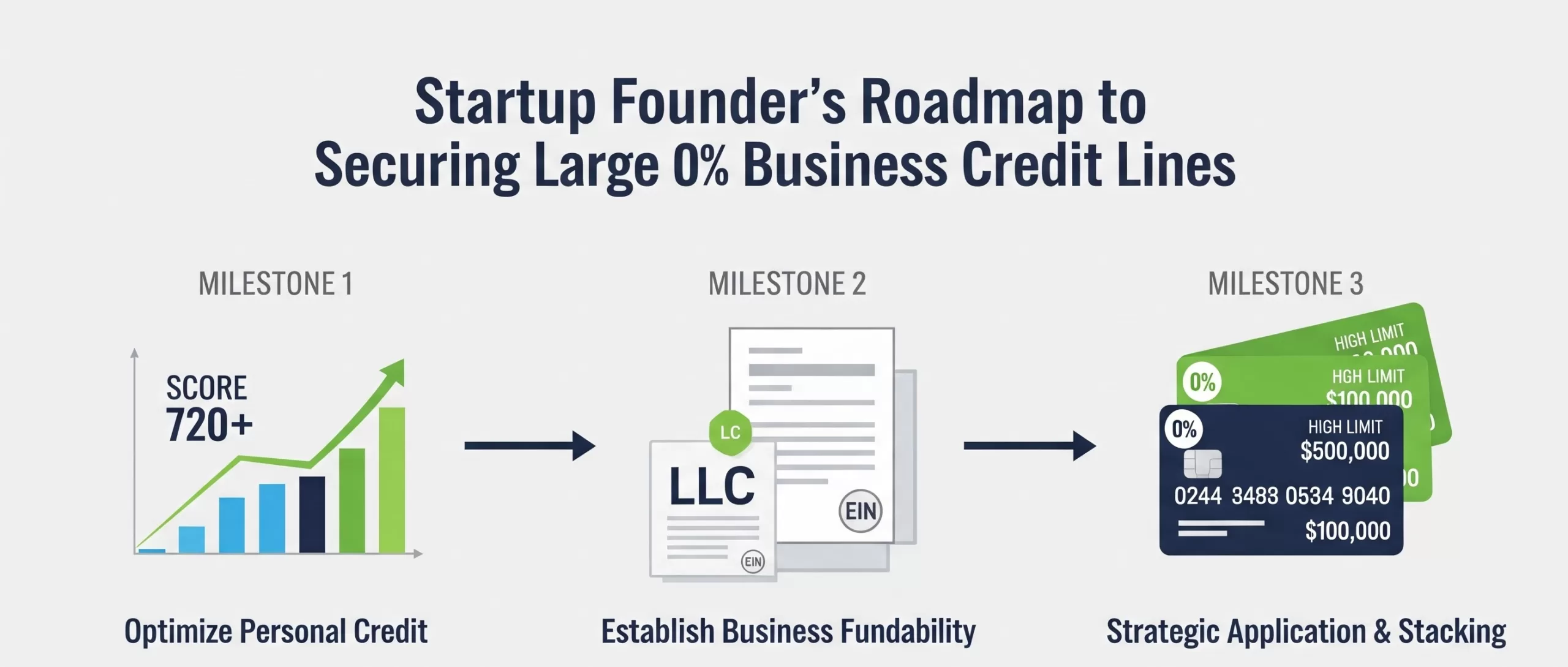

A Tactical Blueprint: The Step-by-Step 0% Business Credit Strategy

Securing a substantial amount of 0% business credit isn’t about applying for a single card; it’s a methodical process that involves preparing your personal and business profiles, then strategically applying for multiple offers. Here’s a tactical roadmap for 2025 to help you succeed.

Step 1: The Personal Credit Foundation

Before you even think about applying for a business credit line, you need to optimize your personal credit. This is the single most important step. Lenders will be looking for a low-risk profile. As Investopedia notes, your FICO score is a snapshot of your creditworthiness. Focus on these key areas:

- Pay Down Debt: Reduce your personal credit card balances. The lower your credit utilization, the better. Aim for under 10% on all cards.

- Address Any Derogatory Marks: Settle or remove any collections, charge-offs, or late payments. Even a single late payment can significantly hurt your chances.

- Don’t Apply for Other Credit: Avoid opening any new personal credit cards or loans in the 3-6 months leading up to your applications. This keeps your credit inquiry count low.

Step 2: Establish Your Business’s Fundability

While your personal credit is the main driver, a well-structured business entity signals legitimacy to lenders. This is where you lay the groundwork for a successful application and, more importantly, for building a business credit profile independent of your personal one. Lenders want to see that you’ve created a separate legal entity. A simple way to get started is by using a reputable service like Northwest Registered Agent to form your LLC or corporation quickly and correctly.

- Register Your Business: Form an LLC or Corporation and obtain a Federal Tax ID Number (EIN). This is your business’s social security number.

- Open a Dedicated Business Bank Account: This is non-negotiable. Lenders want to see a clear separation between your personal and business finances. Our guide to the Best Business Bank Accounts for Startups provides great options, like Mercury which is designed for tech startups.

- Apply for a DUNS Number: A D-U-N-S Number from Dun & Bradstreet is a unique identifier for your business and is required for some lenders and for building a business credit file.

Step 3: The Application Strategy (Fund & Grow)

This is where the magic happens. Instead of applying for one credit card, the strategy involves a calculated process of applying for multiple 0% business credit lines in a short window of time. The goal is to get approved for the maximum amount of credit before the new credit inquiries hit your credit report and lower your score. This can be complex and requires a deep understanding of lender underwriting. This is precisely the service that partners like Fund & Grow specialize in. Instead of navigating this alone, you can leverage their expertise to maximize your approvals.

Access 0% Business Credit Lines with Fund & Grow

Unlock significant 0% interest business credit lines, ranging from $50,000 to $250,000, for your startup or growing business. Fund & Grow specializes in optimizing your credit profile to secure maximum approvals for operational and growth expenses.

- ✅ $50,000 – $250,000 in Credit Lines

- ✅ 0% Interest for 6-18 Months

- ✅ Boost Your Business Credit Score

- ✅ Expert Guidance & Support

- ✅ Ideal for Startups & Small Businesses

Learn how to leverage this powerful funding strategy for your venture.

Working with an expert partner helps you identify the right cards for your profile and manage the application process to get the highest possible limits. They understand which lenders are “personal credit based” and which will be more sensitive to business financials. After approval, you can utilize the funds for payroll, inventory, marketing, and more. For instance, you could use these funds for a payroll loan to cover employee expenses as you wait for revenue to catch up.

Case Studies: How Founders Leverage 0% Offers to Fuel Growth

The 0% business credit strategy isn’t just theory; it’s a proven method used by successful entrepreneurs to scale. These real-world applications demonstrate the power of this approach as a form of strategic debt.

Case Study 1: The SaaS Startup Founder

Jane, a software developer, wanted to build a SaaS application but lacked the seed capital to hire a team. With a personal FICO score of 740, she partnered with a credit expert who helped her secure four different 0% business credit lines from various banks, totaling $110,000. She used this capital over the next 12 months to fund a team of freelance developers and launch her product. By the time the 0% intro period ended, she had secured her first 100 paying customers and a small angel investment. She used the investment to pay off the credit lines in full, having launched her business and proved her model without giving up a single percentage of equity. This is a perfect example of using non-dilutive financing to prove a concept, a key step before you even think about creating a winning investor pitch deck.

Case Study 2: The E-commerce Entrepreneur

Mark ran a small but profitable e-commerce store. His biggest challenge was purchasing inventory for the holiday season without impacting cash flow. He used the 0% business credit strategy to secure $80,000 in credit lines. He used the funds to purchase his inventory in bulk, enabling him to get a significant discount from his suppliers. He then sold the products throughout the holiday season, paid off the credit lines before the promotional period expired, and kept the profits. The interest-free nature of the funding meant his profit margins were higher, and he was able to use the capital to seize a time-sensitive opportunity. This is a common strategy that many e-commerce entrepreneurs employ as an alternative to a traditional fast business loan with minimal paperwork.

Comparison Table: 0% Cards vs. Term Loans for Growth

To help you decide if this strategy is right for you, here is a quick comparison of 0% business credit lines against other common funding methods. This table highlights how a 0% business credit strategy stands apart from traditional term loans and even regular business credit cards.

| Feature | 0% Business Credit Lines | 0% Business Credit Cards | Small Business Term Loan |

|---|---|---|---|

| Typical Funding Amount | $50,000 – $250,000+ | $10,000 – $50,000 | $10,000 – $500,000+ |

| Primary Approval Factor | Personal Credit (FICO 680+) | Personal Credit (FICO 680+) | Business Revenue, Financials, and Collateral |

| Repayment Term | Revolving (open-ended) | Revolving (open-ended) | Fixed (1-10 years) |

| Interest Rate | 0% for 6-18 months, then variable APR (15-25%) | 0% for 6-21 months, then variable APR (15-25%) | Fixed APR (4-30%+) from day one |

| Best Use Case | Startups, working capital, inventory, marketing, and consolidating debt. | Small purchases, day-to-day expenses, and travel. | Major fixed asset purchases, business acquisition, and large-scale expansion. |

| Speed to Funding | Can be 30-90 days, depending on stacking strategy. | Can be instant to 1-2 weeks. | Weeks to months (e.g., SBA loans). For faster options, see National Funding. |

| Impact on Credit | Builds business credit; personal score may fluctuate initially. | Primarily builds personal credit; may impact business score minimally. | Builds business credit; can have a minimal impact on personal credit. |

Beyond 0% Lines: Building Your Business’s Fundability

While a 0% business credit strategy is an incredible tool for early-stage capital, it’s just one piece of the puzzle. The ultimate goal is to build your business’s independent credit profile to the point where it can secure large loans based on its own merit, not just your personal credit score. This is where the initial use of credit lines becomes a foundation for future growth. Every time you responsibly use and repay a business credit line, you’re building a history with major business credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business.

If you have a lower personal credit score, or if you simply want a different path to unsecured funding, there are other strategies and partners that can help. A company like Fundwise Capital specializes in helping businesses with a blend of personal and business credit to get prequalified for up to $150,000 in unsecured funding. It’s an ideal option for those who may not meet the strict 700+ FICO score needed for the aggressive 0% stacking strategy. For more details on what it takes to qualify, check out our guide on the Fundwise Credit Score Requirements for Unsecured Funding.

Prequalify for Unsecured Funding with Fundwise Capital

Get quick access to unsecured business funding without the hassle. Fundwise Capital helps you prequalify for up to $150,000 in capital based on a blend of your personal and business credit, making funding simpler and faster.

- ✅ Prequalify in Minutes

- ✅ Up to $150,000 in Unsecured Funding

- ✅ No Collateral Required for Unsecured Options

- ✅ Streamlined Application Process

- ✅ Solutions for Various Business Stages

See how much funding your business can get prequalified for today!

Why The 0% Business Credit Strategy is a High-ROI Funding Play

The core advantage of using 0% business credit lines is the cost of capital. When you use interest-free funds to invest in growth, every dollar of profit is yours to keep. This is a game-changer for businesses in their early stages that need to invest heavily in marketing, inventory, or hiring without the burden of interest payments. It’s a prime example of strategic debt as a form of startup investment.

By leveraging this strategy, you can:

- Avoid Dilution: You don’t have to give up valuable equity in your company to get the funding you need.

- Maintain Control: You retain complete control over your business decisions without answering to investors.

- Build a Solid Business Credit Profile: This strategy lays the foundation for securing larger, more traditional forms of financing down the line, such as a business line of credit or a term loan.

Frequently Asked Questions About 0% Business Credit

Is a 0% business credit line a business loan?

No, a 0% business credit line is a form of revolving credit, not a term loan. A term loan provides a lump sum of cash upfront with a fixed repayment schedule, while a credit line allows you to draw funds as needed, pay them back, and reuse the credit limit. This makes it more flexible for ongoing expenses. For a deeper look, read our article on Business Line of Credit vs. Term Loan.

What credit score do I need to get 0% business credit?

While some programs may have slightly different requirements, most require a personal FICO score of 680 or higher. For the best chances of securing significant credit limits, a score of 720+ is highly recommended. For those with a lower score, other funding options like a business loan with bad credit may be a better starting point.

Is this a safe funding strategy?

Yes, when done correctly, it is a very safe strategy. The key is to have a clear plan for how you will use the funds and, most importantly, how you will pay them off before the 0% promotional period ends. Many founders use this capital to finance a specific project, which generates revenue that can then be used for repayment. It’s a popular alternative to no doc business loans, which can come with very high interest rates and fees.

How long does it take to get 0% business credit lines?

The timeline can vary. Individual card or line approvals can be fast—sometimes in minutes. However, a full-scale stacking strategy to secure $100,000+ can take several weeks or even a few months of coordinated applications to maximize approvals while minimizing the impact on your credit. This is why working with an expert partner is so valuable for an expedited process. If you need capital faster, check out our guide on the Fastest Business Loans for Startups.

Maximize Rewards with Amex Business Cards

Unlock powerful spending potential and earn valuable rewards with an American Express Business Card. Benefit from introductory 0% APR offers, robust spending power, and features designed for business growth.

- ✅ Generous Welcome Offers

- ✅ Flexible Rewards on Business Spending

- ✅ No Annual Fee Options Available

- ✅ Tools for Expense Management

- ✅ Access to Amex Business Resources

Discover the Amex Business Card that’s right for your company’s financial needs.

Conclusion: Your Path to Interest-Free Capital

Securing 0% business credit lines is one of the smartest moves a startup founder can make. It provides access to significant, non-dilutive capital without the immediate burden of interest, allowing you to invest in growth on your own terms. By focusing on your personal credit foundation and leveraging a strategic approach, you can unlock a powerful funding source that most entrepreneurs don’t even know exists.

If you’re ready to take the next step and see how much 0% interest credit you can qualify for, we highly recommend connecting with an expert. Stop giving away equity or paying high-interest rates, and start using smarter strategies to fund your business.

Ready to Unlock Your 0% Business Credit Lines?

Get a step-by-step roadmap from experts who help founders secure large, interest-free credit lines for growth.

Disclosure: Some of the links on this page are affiliate links. This means we may earn a commission at no extra cost to you if you make a purchase through one of our partners. We only recommend tools we believe will genuinely benefit our audience.