Contractor Financing Guide: Unsecured Funding & Business Credit for Contractors

As a contractor, you know that managing cash flow is the lifeblood of your business. The all-too-common reality is that many projects require significant upfront costs for materials and labor, but payments from clients can be delayed by weeks or even months. This gap often forces contractors to rely on their personal savings or cash flow, which can be a fragile and unsustainable strategy. When you approach traditional banks for a loan, the process can be slow, demanding, and often ends in a denial, as one contractor on a Reddit thread lamented. What if there was a better way to secure the funding you need to grow without relying on a bank’s unpredictable decisions or your personal finances? Learn more about how financing can drive your business forward in this article from Boom & Bucket.

This comprehensive guide is your roadmap to navigating the world of contractor financing. We’ll move beyond traditional loans and explore powerful alternatives like unsecured credit lines, vendor credit, and even specialized SBA loans that are often more accessible to contractors. You’ll learn how to proactively build your business credit score from scratch, and we’ll provide actionable checklists to help you prepare your business for success. Read on to discover the strategies that can free you from cash flow pressures and provide the capital you need to take on bigger, more profitable projects.

Jump to Table of Contents

Table of Contents

- The Problem with Traditional Bank Loans for Contractors

- Unsecured Business Funding: Your Best Alternative

- The Power of Vendor Credit for Contractors

- SBA Loans for Construction Businesses: A Deeper Look

- How to Build Business Credit for Contractors Step-by-Step

- Comparison of Top Contractor Financing Options

- Ready to Secure Your Funding? Final Steps

- Frequently Asked Questions (FAQ)

The Problem with Traditional Bank Loans for Contractors

Traditional banks often have rigid lending criteria that don’t align with the unique financial dynamics of a contracting business. When you apply for a loan, they typically want to see extensive financial history, consistent W-2 income, and a high personal credit score. For many contractors, especially those who are newly established or operating as sole proprietors, this can be a significant barrier. The cyclical nature of projects and reliance on delayed client payments means your cash flow might not look consistent on paper, which can be a red flag for a conservative loan officer.

Moreover, banks may be hesitant to lend to contractors due to the perceived “risk” of the construction industry. Project delays, unexpected costs, and a lack of tangible collateral can make them wary. This is why many contractors find themselves in a bind, with their only option being to fund projects out of their own pocket. This not only puts a strain on your personal finances but also limits your ability to take on multiple, larger projects simultaneously. You can find more information about how different funding types work in our article on business credit vs. business loans.

Unsecured Business Funding: Your Best Alternative

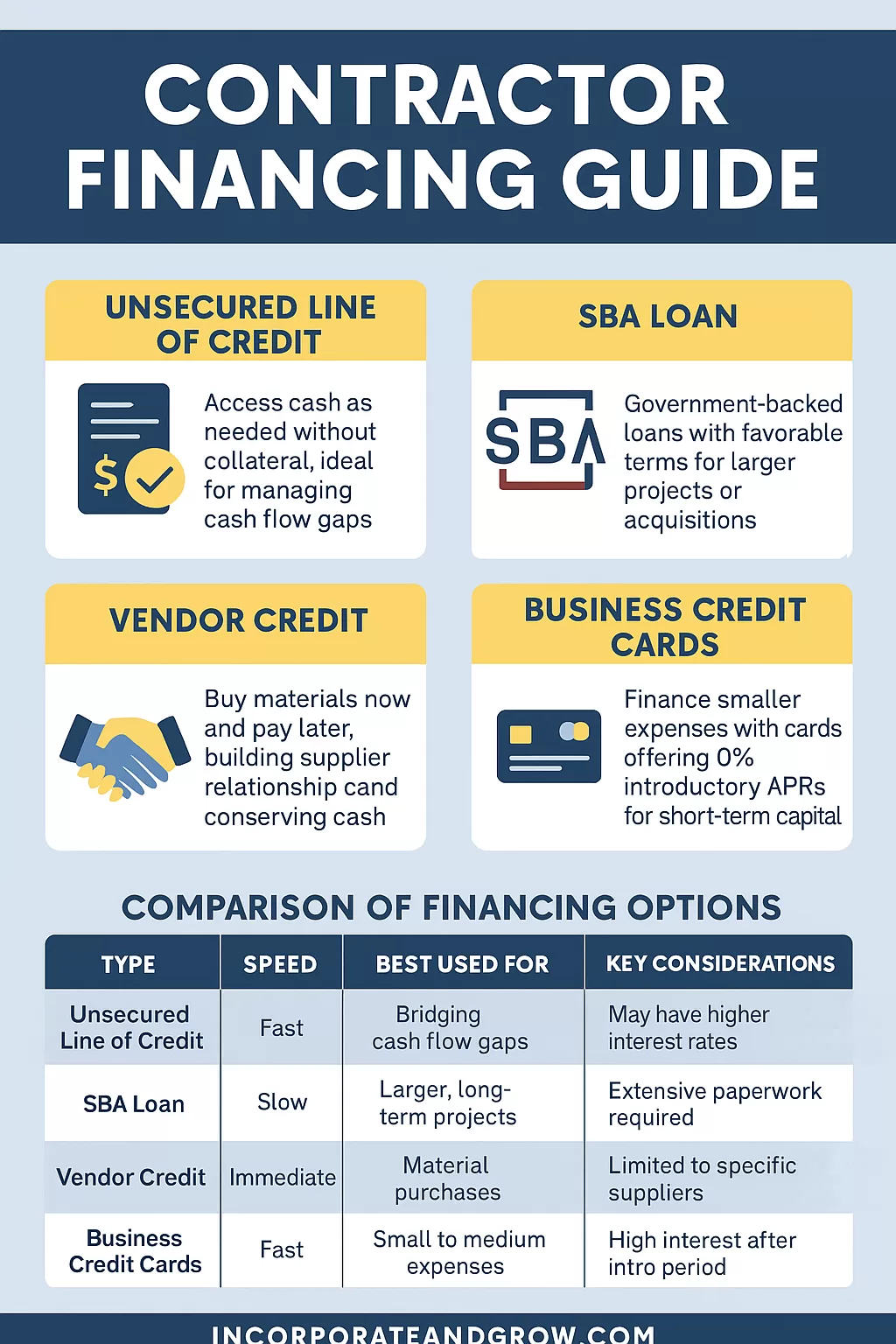

Unsecured business funding is often the ideal solution for contractors who struggle with traditional loans. This type of financing doesn’t require you to put up personal assets or property as collateral. Instead, lenders base their decision on factors like your business’s revenue, cash flow, and personal credit history. For a more detailed look at what a line of credit is, check out this article from Investopedia.

The most common forms of unsecured funding for contractors include business credit lines and business credit cards with a 0% introductory APR. These options provide the flexibility to draw funds as needed, pay them back, and draw again, making them perfect for managing irregular project-based expenses. This is a far cry from a traditional term loan, which delivers a lump sum that starts accruing interest immediately.

- Unsecured Business Lines of Credit: Think of this as a financial safety net. You’re approved for a maximum amount, but you only pay interest on what you use. This is perfect for bridging the gap between project expenses and client payments, helping you avoid cash flow crunches.

- Business Credit Cards with 0% Intro APR: Many business credit cards offer a promotional period where you can make purchases without paying interest for 6, 12, or even 18 months. This is essentially free capital that you can use to buy materials or cover payroll, giving you ample time to get paid by your clients. Our guide on business loans vs. business credit cards provides a deeper dive into these options.

Prequalify for Unsecured Funding with Fundwise Capital

Get quick access to unsecured business funding without the hassle. Fundwise Capital helps you prequalify for up to $150,000 in capital based on a blend of your personal and business credit, making funding simpler and faster.

- ✅ Prequalify in Minutes

- ✅ Up to $150,000 in Unsecured Funding

- ✅ No Collateral Required for Unsecured Options

- ✅ Streamlined Application Process

- ✅ Solutions for Various Business Stages

See how much funding your business can get prequalified for today!

The Power of Vendor Credit for Contractors

Vendor credit, also known as “trade credit,” is a powerful and often overlooked tool for managing cash flow. This is where your suppliers and distributors extend you a line of credit to purchase materials now and pay for them later, typically within 30, 60, or 90 days. This is a game-changer for contractors because it allows you to get the supplies you need to start a job without using up your own cash.

Building strong relationships with your suppliers and consistently paying on time not only helps your business run smoothly but also starts to build a credit profile for your business. Many suppliers report your payment history to business credit bureaus like Dun & Bradstreet, Experian Business, and Equifax Business. This is a foundational step for building your business credit score, separate from your personal credit. This strategy is also a key component in our article, Building Business Credit for Startups: A Step-by-Step Guide. For more information on the benefits and alternatives of contractor financing, see this guide from Moon Invoice.

“Vendor credit is a long-standing, often interest-free way to fund material purchases, directly supporting the project life-cycle without a bank in sight.”

SBA Loans for Construction Businesses: A Deeper Look

While many contractors may feel discouraged by the SBA loan process, these government-backed loans can be a phenomenal source of capital, especially for established construction businesses. The key is understanding that SBA loans are not direct loans from the government; rather, they are loans provided by banks and other lenders that are partially guaranteed by the U.S. Small Business Administration (SBA). This guarantee reduces the risk for the lender, making them more willing to approve loans for small businesses. You can find more information about construction loans in this detailed guide from Buildern.

For construction and contracting businesses, the most common type of SBA loan is the 7(a) program. This loan can be used for a wide range of purposes, including:

- Acquiring new equipment or vehicles.

- Purchasing commercial real estate for an office or shop.

- Providing long-term working capital to cover operational expenses.

- Refinancing existing business debt.

While SBA loans can have a lengthy application process and require substantial documentation, the benefits are significant: lower interest rates, longer repayment terms (up to 25 years for real estate), and higher funding limits (up to $5 million) compared to other financing options. To get started, you can use our SBA loan checklist to ensure you have all your documents in order.

How to Build Business Credit for Contractors Step-by-Step

Building business credit is a critical, long-term strategy that provides you with financial independence from your personal credit. For contractors, a strong business credit profile can lead to higher funding approvals, better loan terms, and more favorable vendor relationships. For an in-depth understanding of how business credit scores work, read this article from Forbes Advisor. Here’s a step-by-step guide to get started:

- Formally Establish Your Business: You cannot build business credit without a legally recognized business entity. If you’re a sole proprietor, consider forming an LLC or a Corporation. This separates your personal liability from your business and is the first step toward getting an EIN. Check out our guide on LLC vs. Sole Proprietorship for Funding to learn more.

- Get an EIN and DUNS Number: An Employer Identification Number (EIN) from the IRS is like a Social Security Number for your business. A DUNS number from Dun & Bradstreet is a unique nine-digit number used by lenders to identify your business. Both are essential for creating a business credit file.

- Open a Dedicated Business Bank Account: Keep your personal and business finances separate. Use a dedicated business bank account for all income and expenses. This creates a clear financial history that lenders will want to see. Our article on the best business bank accounts for startups can help you choose the right one.

- Secure Vendor Credit That Reports: As mentioned earlier, establishing vendor accounts that report your payment history to business credit bureaus is a cornerstone of building business credit. Seek out suppliers and distributors that offer “Net-30” or “Net-60” terms and pay your invoices on time, every time.

- Get a Business Credit Card: A business credit card that reports to business credit bureaus is a powerful tool for building credit. Even if you’re approved for a small limit initially, using it responsibly and paying the balance off each month will quickly improve your business credit profile.

Access 0% Business Credit Lines with Fund & Grow

Unlock significant 0% interest business credit lines, ranging from $50,000 to $250,000, for your startup or growing business. Fund & Grow specializes in optimizing your credit profile to secure maximum approvals for operational and growth expenses.

- ✅ $50,000 – $250,000 in Credit Lines

- ✅ 0% Interest for 6-18 Months

- ✅ Boost Your Business Credit Score

- ✅ Expert Guidance & Support

- ✅ Ideal for Startups & Small Businesses

Learn how to leverage this powerful funding strategy for your venture.

Comparison of Top Contractor Financing Options

| Funding Type | Best For | Key Requirements | Funding Speed | Pros & Cons |

|---|---|---|---|---|

| Unsecured Line of Credit | Bridging cash flow gaps and unexpected expenses | Good personal credit (680+), established business revenue | Fast (1-3 business days) | ✅ Flexible, only pay interest on what you use ❌ May have higher interest rates than traditional loans |

| SBA Loan (7a) | Large projects, equipment, or real estate purchases | Good personal credit, 2+ years in business, solid financial history | Slow (weeks to months) | ✅ Low rates, long terms, high limits ❌ Lengthy application, extensive paperwork |

| Vendor/Trade Credit | Material and supply purchases | Strong relationship with supplier, clean payment history | Immediate | ✅ Interest-free (if paid on time), builds business credit ❌ Limited to specific suppliers, short payment windows |

| Business Credit Card (0% APR) | Small to medium project expenses, short-term cash flow | Good personal credit (680+), decent revenue | Fast (immediate upon approval) | ✅ “Free” capital for intro period, builds business credit ❌ Limited credit limits, high interest after intro period |

| Invoice Factoring | Immediate access to cash from unpaid invoices | Outstanding invoices from creditworthy clients | Fast (24-48 hours) | ✅ Quick access to cash, improves cash flow ❌ High fees, you don’t receive full invoice value |

For a more detailed look at the pros and cons of these options, see our related article on business lines of credit vs. term loans.

Get Fast Business Funding with National Funding

Need capital quickly? National Funding specializes in providing fast, flexible business loans and merchant cash advances, even with minimal paperwork. Get the funds you need to seize opportunities and grow your business.

- ✅ Funding in as Fast as 24 Hours

- ✅ Flexible Repayment Options

- ✅ Solutions for Various Credit Profiles

- ✅ Dedicated Business Funding Specialists

- ✅ Focus on Small to Medium-Sized Businesses

Apply today and get pre-qualified for the capital your business needs to thrive.

Ready to Secure Your Funding? Final Steps

Securing contractor financing is more than just applying for a loan; it’s about building a robust financial foundation for your business. By taking the time to separate your personal and business finances, establish vendor credit, and actively build a business credit score, you’re not just solving a short-term cash flow problem—you’re future-proofing your entire operation.

Don’t let the frustration of being denied a traditional bank loan deter you. The world of small business financing has evolved, and there are now numerous paths to get the capital you need. By strategically leveraging tools like unsecured credit lines and vendor credit, you can take control of your finances and focus on what you do best: building and growing your business.

Prequalify for Unsecured Funding with Fundwise Capital

Get quick access to unsecured business funding without the hassle. Fundwise Capital helps you prequalify for up to $150,000 in capital based on a blend of your personal and business credit, making funding simpler and faster.

- ✅ Prequalify in Minutes

- ✅ Up to $150,000 in Unsecured Funding

- ✅ No Collateral Required for Unsecured Options

- ✅ Streamlined Application Process

- ✅ Solutions for Various Business Stages

See how much funding your business can get prequalified for today!

Frequently Asked Questions (FAQ)

What is the best type of financing for a new contractor?

For new contractors, a great place to start is with a business credit card that has a 0% introductory APR period. This gives you access to a flexible line of credit without paying interest. Concurrently, you should focus on building relationships with suppliers to secure vendor credit, which will help with material costs.

How can I get contractor financing with a low personal credit score?

If your personal credit score is a concern, you can explore options that rely more on business revenue and cash flow. Merchant cash advances and invoice factoring are two options, though they can have high fees. The best long-term strategy is to focus on building your business credit score from scratch, as outlined in this guide. We have a detailed guide on business loans with bad credit that might be helpful.

Do contractors need a D-U-N-S number?

Yes, while not always required for every lender, a D-U-N-S number is essential for building a formal business credit file with Dun & Bradstreet. Many large companies and government agencies require a D-U-N-S number before they will do business with you.

Disclosure: Some of the links on this page are affiliate links. This means we may earn a commission at no extra cost to you if you make a purchase through one of our partners.