SBA 7(a) vs SBA 504 Loans: Which Is Right for Your Business in 2025?

Navigating the world of small business funding can be complex, especially when considering government-backed options like those offered by the U.S. Small Business Administration (SBA). For many founders, the choice often comes down to two primary programs: the **SBA 7(a) loan** and the **SBA 504 loan**. Both offer significant advantages over traditional bank loans, but they serve very different purposes and have distinct requirements.

In this comprehensive 2025 guide, we’ll break down the key differences between the SBA 7(a) and SBA 504 loan programs to help you determine which is the best fit for your business’s unique needs and goals. We’ll explore their uses, eligibility criteria, and how they can fuel your growth, while also considering alternative funding paths.

Understanding SBA Loans: Your Gateway to Capital

SBA loans are not direct loans from the government. Instead, they are loans provided by private lenders (like banks and credit unions) that are partially guaranteed by the SBA. This government guarantee reduces the risk for lenders, making them more willing to provide financing to small businesses that might not otherwise qualify for conventional loans.

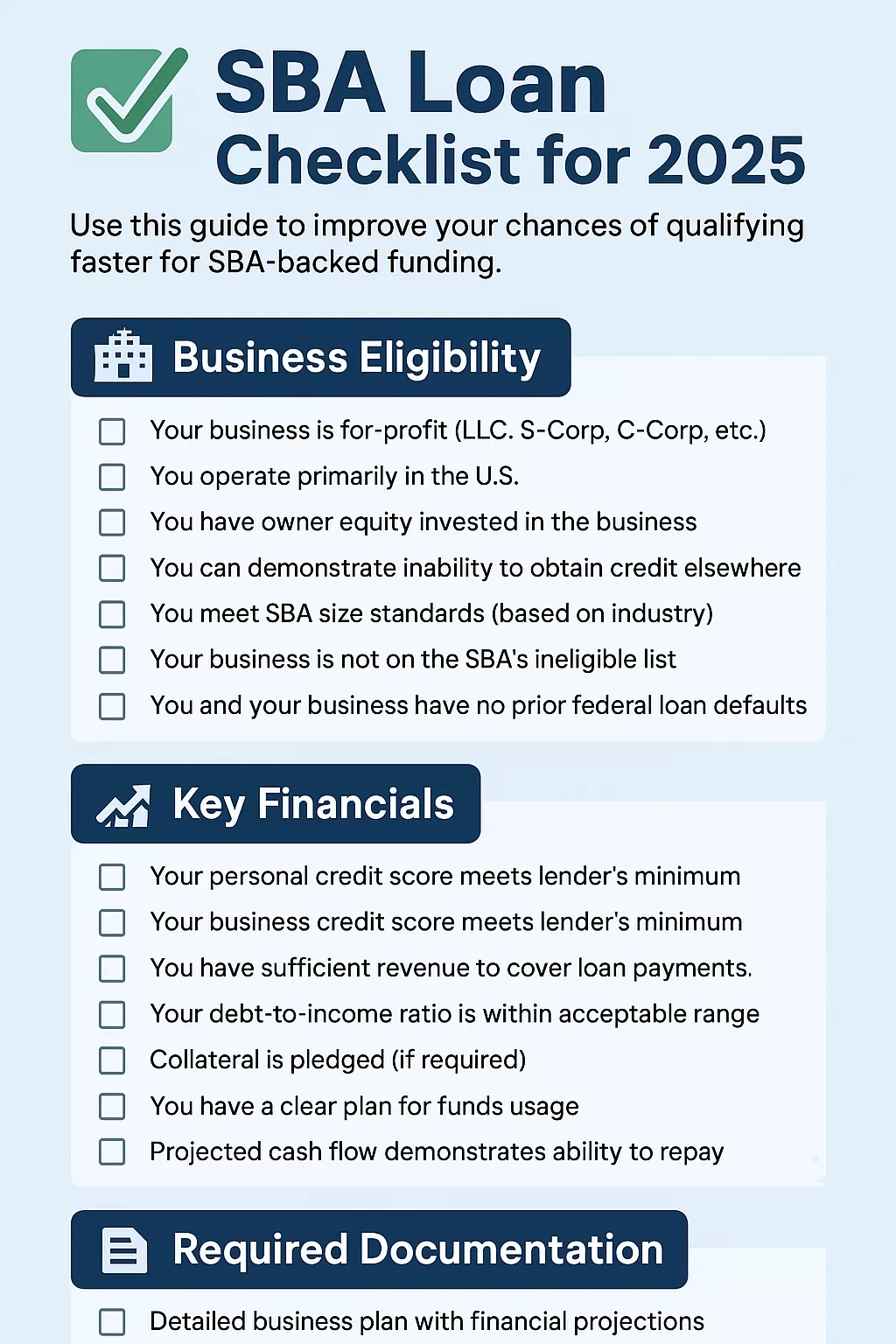

The SBA’s mission is to support small businesses, and its loan programs are designed to provide access to capital for a wide range of needs, from working capital to real estate and equipment purchases. Understanding the nuances of each program is critical for a successful application. For a general overview of what you’ll need, check our SBA Loan Checklist 2025 and your broader Business Loan Approval Checklist.

SBA 7(a) Loan: The Flexible Choice

The SBA 7(a) loan program is the SBA’s primary and most flexible loan program. It’s often used for a broad range of general business purposes, making it a popular choice for diverse small business needs.

Typical Uses for SBA 7(a) Loans:

- Working capital (e.g., inventory, operating expenses)

- Purchasing land or real estate (including renovations)

- Acquiring equipment, machinery, or furniture

- Refinancing existing business debt

- Purchasing an existing business or franchise

Pros of SBA 7(a) Loans:

- Highly flexible use of funds.

- Long repayment terms (up to 10 years for working capital, 25 years for real estate).

- Lower down payments compared to conventional loans.

- Competitive interest rates due to the government guarantee.

Cons of SBA 7(a) Loans:

- Can have a lengthy application and approval process.

- Requires substantial documentation.

- Personal guarantees are typically required.

For more detailed information, you can always refer to the official SBA 7(a) loans page.

SBA 504 Loan: Real Estate & Equipment Focused

The SBA 504 loan program is designed specifically for fixed-asset projects. This means it’s ideal for businesses looking to purchase or renovate commercial real estate, or to acquire major machinery and equipment. This loan is a partnership among three parties: a private sector lender, a Certified Development Company (CDC), and the borrower.

Typical Uses for SBA 504 Loans:

- Purchasing existing buildings or land

- Financing the construction of new facilities or modernizing existing ones

- Acquiring long-term machinery or equipment

- Improving land, streets, utilities, or existing facilities

Pros of SBA 504 Loans:

- Low down payment (often 10%, compared to 20-30% for conventional loans).

- Long repayment terms (10, 20, or 25 years).

- Fixed interest rates on the CDC portion of the loan.

- Helps small businesses acquire assets that typically require significant upfront capital.

Cons of SBA 504 Loans:

- Funds can only be used for fixed assets; no working capital.

- Requires a larger loan amount to justify the process.

- More complex structure involving a bank and a CDC.

Learn more about the program on the SBA 504 loans official website.

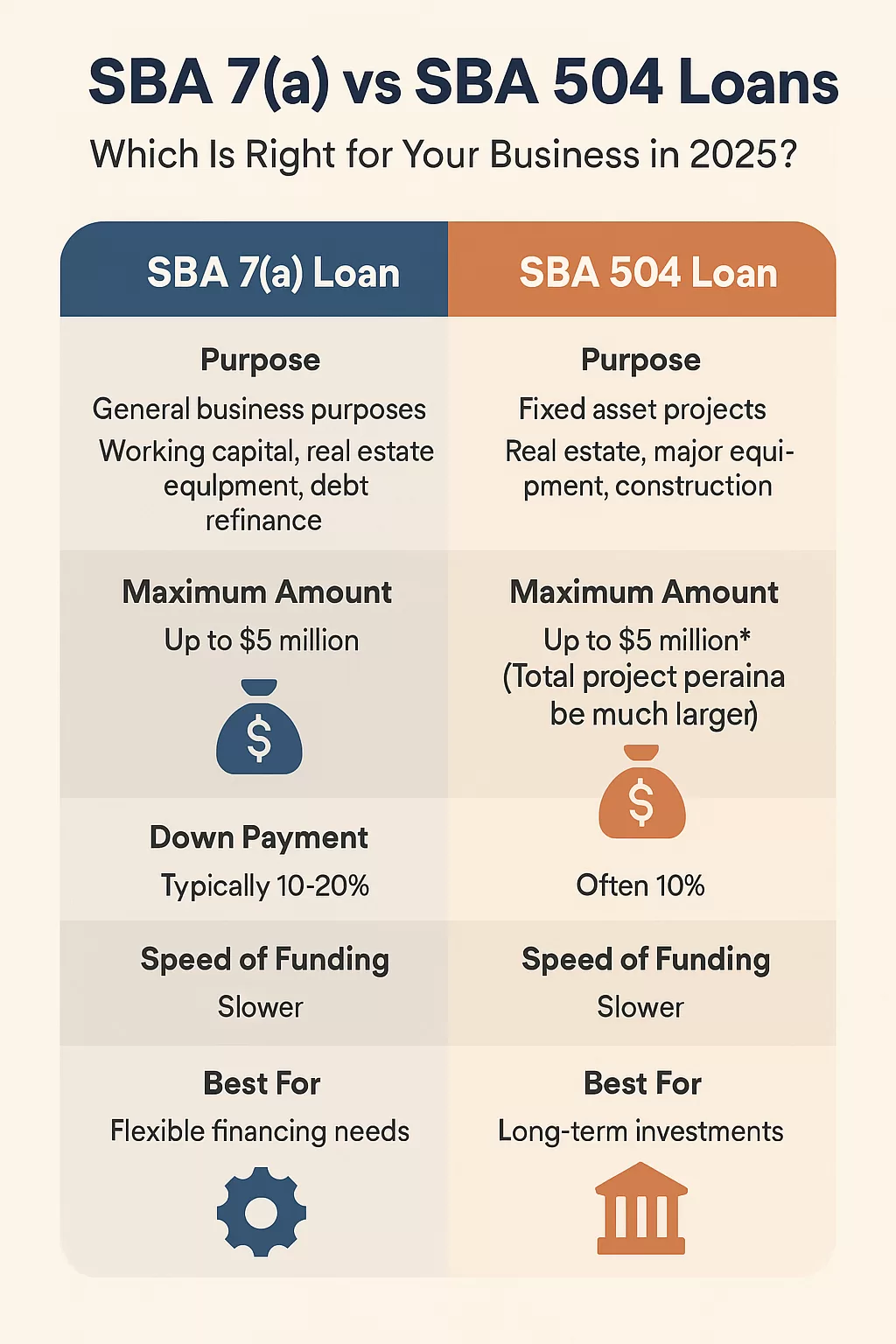

SBA 7(a) vs. SBA 504: Side-by-Side Comparison

To help you quickly grasp the core differences, here’s a comparison table:

| Feature | SBA 7(a) Loan | SBA 504 Loan |

|---|---|---|

| Primary Purpose | General business purposes (working capital, real estate, equipment, debt refinance, business acquisition) | Fixed asset projects (real estate, major equipment, construction) |

| Maximum Loan Amount | Up to $5 Million | Up to $5 Million (CDC portion), but total project can be much larger |

| Structure | One loan from a single lender (bank/credit union) | Three-part structure: 50% from bank, 40% from CDC (SBA-backed), 10% from borrower |

| Down Payment | Typically 10-20% (can vary) | Often 10% (for established, healthy businesses) |

| Interest Rate | Variable or fixed, negotiated with lender (capped by SBA) | Variable on bank portion, fixed on CDC portion |

| Collateral | Required when available; personal guarantee always | Project assets serve as collateral; personal guarantee may be required |

| Speed of Funding | Can be slow (weeks to months) | Often slower due to complex structure (months) |

| Eligibility Focus | Broad range of small businesses | Businesses creating or retaining jobs, or meeting public policy goals |

Which SBA Loan is Right for Your Business?

Choosing between an SBA 7(a) and 504 loan depends entirely on your specific needs:

- Choose SBA 7(a) if: You need working capital, want to refinance debt, purchase an existing business, or require funding for a mix of purposes. Its flexibility makes it suitable for diverse operational and expansion needs.

- Choose SBA 504 if: Your primary goal is to acquire or build commercial real estate, or purchase heavy, long-term equipment. It’s designed to help businesses make significant fixed-asset investments with a lower down payment.

Always consult with an SBA-approved lender or a financial advisor to discuss your unique situation and determine the best fit.

Alternatives to SBA Loans: When Speed or Flexibility is Key

While SBA loans offer fantastic terms, their application process can be lengthy and stringent. If your business needs capital faster, or if you don’t meet strict SBA requirements, consider these alternatives:

Need Fast Capital Without the SBA Red Tape?

For established businesses needing quick access to capital for working expenses, inventory, or urgent opportunities, traditional SBA loans might be too slow. Consider National Funding. They specialize in fast business loans with minimal paperwork, offering funding in as little as 24 hours for qualified businesses. It’s an excellent option for immediate needs when SBA timelines aren’t feasible.

Exploring Unsecured Funding & Business Credit?

If SBA loans aren’t a fit for your credit profile or specific funding needs, focusing on building strong business credit or securing unsecured lines can be a powerful alternative. Learn about Fundwise Capital for unsecured funding and explore how to grow your business credit with programs like Fund & Grow Business Credit.

These options can provide capital with different eligibility criteria, often focusing on business revenue or credit-building strategies rather than traditional collateral requirements.

Preparing Your Business for Any Loan Application

No matter which loan path you choose, having your financial house in order is paramount. Lenders, including SBA-approved ones, scrutinize your financial records to assess risk. Clean and consistent bookkeeping is a green flag that can significantly speed up your approval process.

Streamline Your Financials with Trusted Tools:

Ensuring your financials are impeccable for loan applications, especially SBA loans, is critical. Consider using professional bookkeeping and accounting tools:

- Bench: Offers done-for-you bookkeeping services by a team of professionals, ensuring accurate and compliant financial records that lenders love to see.

- Xero: Provides robust cloud accounting software for modern businesses, allowing you to track expenses, manage invoices, and monitor cash flow in real-time, making financial reporting a breeze.

A solid small business bookkeeping and payroll guide can set you up for success.

Key Takeaways for 2025

- SBA 7(a) is highly versatile for general business needs and working capital.

- SBA 504 is specifically for fixed assets like real estate and major equipment.

- Both offer competitive terms but often involve a lengthier application process than alternative lenders.

- Your specific funding purpose should dictate your choice between 7(a) and 504.

- Always keep impeccable financial records using tools like Bench or Xero to ease any loan application process.

FAQs about SBA 7(a) and 504 Loans

What is the main difference between an SBA 7(a) and 504 loan?

The main difference lies in their purpose. The SBA 7(a) loan is flexible and can be used for various general business purposes, including working capital, real estate, equipment, and debt refinancing. The SBA 504 loan, however, is specifically for fixed assets like real estate, construction, or major equipment purchases.

Can I get both an SBA 7(a) and 504 loan?

It’s generally not possible to use both types of loans for the same project or simultaneously for conflicting purposes. However, a business might qualify for different SBA loans for separate, distinct projects or needs over time, provided they meet all eligibility requirements for each.

What are the typical interest rates for SBA 7(a) and 504 loans in 2025?

For SBA 7(a) loans, interest rates are negotiated with the lender but are capped by the SBA (typically prime rate plus a spread). For SBA 504 loans, the bank’s portion will have a variable rate, while the CDC portion has a fixed interest rate tied to U.S. Treasury bond rates at the time of funding, offering stability for that part of the loan.

How long does it take to get an SBA 7(a) or 504 loan?

Both loan programs can involve a lengthy process compared to private online lenders. SBA 7(a) loans typically take weeks to a few months for approval and funding. SBA 504 loans, due to their complex structure involving a bank and a CDC, can often take several months to complete the process.

Final Thoughts: Power Your Growth with the Right SBA Choice

Choosing between an SBA 7(a) and SBA 504 loan is a strategic decision that can significantly impact your business’s future. By understanding their core differences and aligning them with your specific funding objectives, you can leverage these powerful government-backed programs to acquire essential assets, manage operations, or expand your reach.

Remember to prepare diligently, explore all your options—including faster alternatives for urgent needs—and build a strong financial foundation to make your business lendable.

Ready to explore your funding options? Don’t wait for your next growth opportunity to pass you by.