1. Introduction: Your Funding Path Starts Here

As a startup founder or small business owner, navigating the financial landscape can feel like a labyrinth. You’ve got big ideas, but bringing them to life often requires capital. The question isn’t just “Where can I get money?” but “What’s the best funding option for my specific needs?” Two common contenders often emerge: the business loan vs business credit card. While seemingly similar, these tools serve distinct purposes and come with their own sets of advantages and disadvantages.

The year 2025 presents a unique financial environment for entrepreneurs. Factors such as evolving interest rates, the proliferation of alternative lenders, and the inherent challenges faced by early-stage ventures significantly influence capital acquisition strategies. The current economic climate, marked by fluctuating interest rates, directly impacts the borrowing costs associated with both traditional loans and business credit cards. This necessitates a more nuanced understanding of each option’s true cost and suitability.

Furthermore, the financial technology (fintech) sector has diversified the lending landscape beyond conventional banks, offering more tailored and accessible solutions for startups that might not meet stringent traditional criteria. This expansion of options, while beneficial, also adds complexity to the decision-making process. Startups frequently grapple with limited operating history, a lack of substantial collateral, and a heavy reliance on the founder’s personal credit score, making the choice of financing particularly critical. (Source: NerdWallet).

This comprehensive guide aims to empower founders to choose the smartest financing tool for their situation, whether seeking significant growth capital or managing daily cash flow. It will become evident that the decision is often not an either-or proposition, but rather a strategic understanding of how to leverage both business loans and business credit cards in tandem to fuel a startup’s growth in 2025 and beyond. (Source: Investopedia).

—

—

Table of Contents

- 1. Introduction: Your Funding Path Starts Here

- 2. Understanding Business Loans: A Deep Dive for Founders

- 3. Understanding Business Credit Cards: Flexibility for Modern Startups

- 4. The Ultimate Comparison: Business Loan vs. Business Credit Card in 2025

- 5. Pros & Cons: An Exhaustive Breakdown of Each Funding Tool

- 6. Strategic Application: When to Leverage Each Funding Option

- 7. Building Business Credit Faster: Which Tool Propels Your Profile?

- 8. Top Lenders & Business Credit Cards for Startups in 2025

- 9. Optimizing Your Funding Strategy: The Power of Combined Use

- 10. Frequently Asked Questions (FAQ)

- Conclusion: Empower Your Startup’s Financial Future

- Disclosure Statement

—

2. Understanding Business Loans: A Deep Dive for Founders

A business loan represents a sum of money borrowed from a lender—which could be a traditional bank, an online lending platform, or a government-backed institution—that the borrower agrees to repay, typically with interest, over a predetermined period. This financial instrument functions as a debt obligation, where the principal amount is disbursed upfront, and repayment occurs through a series of fixed installments.

Detailed Types of Business Loans

Business loans come in various forms, each designed to meet specific financial needs:

- Traditional Term Loans: These are perhaps the most straightforward. A lump sum is provided upfront, and the borrower repays it with fixed installments over a specific term, which can range from short-term (e.g., 1-3 years) to long-term (e.g., 5-10 years or more). Short-term loans often come with higher interest rates but are quicker to approve, while long-term loans offer lower monthly payments due to extended repayment periods.

- Lines of Credit (LOC): Unlike a term loan, a business line of credit offers a flexible, revolving borrowing option. Businesses can draw funds up to a certain limit, repay the amount, and then re-draw as needed. Interest is only paid on the amount actively used, making it ideal for managing ongoing working capital needs or unexpected expenses.

- SBA Loans: These are government-backed loans facilitated by the Small Business Administration (SBA). They are known for offering favorable terms, including lower interest rates and longer repayment periods, making them highly attractive for established small businesses seeking growth capital. However, the application process for SBA loans is typically more extensive and can involve longer approval timelines, sometimes stretching into weeks or even months. More information can be found on the SBA.gov website.

- Equipment Loans: Specifically designed for purchasing machinery, vehicles, or specialized technology, equipment loans are often secured by the very equipment being purchased. This collateralization can lead to more favorable interest rates compared to unsecured loans.

- Invoice Financing/Factoring: For businesses that frequently issue invoices to clients and experience delays in payment, invoice financing allows them to get immediate cash by selling their outstanding invoices to a third party at a discount. This provides quick access to cash flow, particularly useful for service-based businesses.

- Merchant Cash Advances (MCAs): An MCA provides a lump sum in exchange for a percentage of future credit card sales. While offering extremely fast access to capital, MCAs are typically very high-cost and should generally be considered only for specific, urgent scenarios where other options are not viable.

Interest Rates and APR Ranges (2025 Context)

The Annual Percentage Rate (APR) for business loans in 2025 can vary significantly based on the loan type, the lender, and the borrower’s creditworthiness. Traditional bank term loans for well-established businesses might see APRs ranging from 6% to 15%. Online lenders, often more accessible to startups, may offer loans with APRs from 15% to 30% or higher, reflecting the increased risk associated with newer businesses or those with less robust financial histories. Secured loans, backed by collateral, typically command lower interest rates than unsecured loans due to reduced risk for the lender.

While the advertised APR is a primary consideration, a deeper examination reveals that the overall cost of a business loan can be significantly influenced by additional charges such as origination fees, closing costs, and potential prepayment penalties. For a startup operating with lean margins, an unforeseen 5% origination fee on a loan effectively reduces the usable capital from day one, directly impacting their immediate operational budget. This necessitates a comprehensive review of all associated costs to accurately gauge the true financial commitment, ensuring that founders look beyond just the percentage rate to understand the total financial burden.

Comprehensive Qualification Criteria

Securing a business loan generally requires a more extensive application process and adherence to stricter qualification criteria compared to business credit cards:

- Time in Business: Most lenders require a minimum operating history, often ranging from 6 months to 2 years, to demonstrate business viability.

- Annual Revenue: Lenders typically look for a certain level of consistent revenue, with common thresholds ranging from $50,000 to $250,000 or more, depending on the loan amount and type.

- Personal Credit Score: For early-stage startups, where business credit is still nascent, the founder’s personal credit score (e.g., FICO score) plays a crucial role in the approval process and in determining interest rates.

- Business Credit Score: As a business matures, its own credit score (e.g., Paydex, Intelliscore, FICO Small Business Scoring Service) becomes increasingly important. Lenders assess this to understand the business’s payment history and financial reliability.

- Collateral Requirements: For larger loans or businesses with limited credit history, lenders may require collateral (e.g., real estate, equipment, accounts receivable) to secure the loan, mitigating their risk.

- Business Plan & Financials: A detailed business plan outlining projections and repayment strategies, along with comprehensive financial statements (profit & loss statements, balance sheets, cash flow statements), are often mandatory to demonstrate financial health and repayment capacity.

Approval Timelines

The speed of loan approval varies significantly. Online lenders can often approve and disburse funds within days, sometimes even within 24-48 hours for certain products. In contrast, traditional bank loans and SBA loans typically involve a more rigorous underwriting process, which can extend approval and funding times to several weeks or even months.

Business loans are ideally suited for large, one-time expenditures that require a substantial lump sum and a predictable, long-term repayment structure. This includes significant investments like purchasing equipment, expanding operations, undertaking major hiring initiatives, or acquiring another business. They provide financial stability through fixed payments and generally offer lower interest rates for larger principal amounts compared to credit cards, especially for well-qualified borrowers.

—

3. Understanding Business Credit Cards: Flexibility for Modern Startups

A business credit card provides a revolving line of credit specifically tailored for business expenses. Unlike a loan, which typically provides a lump sum upfront, a credit card offers a credit limit that can be spent up to, and as payments are made, that credit becomes available again for future use. This continuous access to funds, up to the approved limit, defines its revolving nature. (Source: Investopedia).

Key Features & Benefits

Business credit cards come with a suite of features that can be particularly advantageous for startups:

- 0% Introductory APR: Many business credit cards offer an introductory period (e.g., 12-18 months) during which no interest is charged on purchases or balance transfers. This can be a powerful tool for cash flow management, allowing a startup to make necessary purchases and repay them without incurring interest for an extended period, providing crucial breathing room during early growth stages.

- Rewards Programs: A significant draw of business credit cards is their rewards programs, which often include cashback, travel points, or specific category bonuses (e.g., extra points on office supplies or advertising spend). These rewards can effectively offset business expenses, adding tangible value back to the company.

- Employee Cards: Most business credit card accounts allow the primary cardholder to issue additional cards to employees. This feature simplifies expense tracking, enables setting individual spending limits, and streamlines overall financial management for the business.

- Fraud Protection: Major credit card networks provide robust fraud protection, safeguarding business finances against unauthorized transactions.

- Perks & Benefits: Beyond rewards, many cards offer additional benefits such as travel insurance, purchase protection, extended warranties on purchased items, and access to business services or discounts.

Streamlined Approval Process

The application process for a business credit card is generally much quicker and less intensive than for a business loan. Approvals can often be granted within days, sometimes even instantly for online applications. For startups, lenders primarily focus on the business owner’s personal credit score, as the business itself may not yet have a substantial credit history. While some basic revenue figures or time in business may be requested, the documentation requirements are significantly less burdensome compared to a loan application.

APR After Introductory Period (2025 Context)

While the 0% introductory APR period is a compelling feature, it is critical for founders to understand that interest rates can jump significantly once this period expires. Business credit card APRs are typically variable and can range from 15% to 30% or even higher, making carrying a balance expensive if not managed carefully.

The 0% introductory APR serves as more than just a cost-saving measure; it functions as a strategic cash flow management mechanism. For a nascent startup, this period allows for investment in critical areas like marketing, inventory, or operational infrastructure without the immediate burden of interest, thereby providing a window to generate revenue and establish a stable financial footing. Concurrently, the consistent and timely repayment of a business credit card balance is often reported to business credit bureaus more readily than some smaller loans, making it an accessible and potent instrument for rapidly building a distinct business credit profile from inception. This dual advantage of cash flow optimization and accelerated credit establishment is often underestimated by new entrepreneurs. Therefore, startups are well-advised to maximize the utility of the 0% introductory period for strategic, revenue-generating investments and to prioritize diligent, on-time payments to cultivate robust business credit.

Business credit cards are ideally suited for short-term expenses, managing day-to-day liquidity, covering variable expenses, and separating business and personal finances. They are excellent tools for managing short-term liquidity, covering variable expenses, and separating business and personal finances. They provide crucial tools for managing short-term liquidity, covering variable expenses, and separating business and personal finances. Their flexibility and speed of access make them invaluable for the dynamic needs of a startup.

—

4. The Ultimate Comparison: Business Loan vs. Business Credit Card in 2025

To provide a clear and concise overview, the following table offers a detailed side-by-side comparison of business loans and business credit cards across critical dimensions relevant to startup founders in 2025. This comprehensive breakdown allows for a quick assessment of which financing tool aligns best with specific business needs and circumstances. (Source: NerdWallet).

| Feature | Business Loan | Business Credit Card |

|---|---|---|

| Funding Type | Lump sum / Installment debt | Revolving credit |

| Typical Funding Limits | High (e.g., $5,000 – $5 Million+) | Lower (e.g., $1,000 – $100,000) |

| APR Ranges (2025) | 6% – 30%+ (varies by type/lender/credit) | 0% Intro, then 15% – 30%+ (variable) |

| Approval Time | Weeks to Months (traditional/SBA); Days (online) | Days to Instant |

| Flexibility of Use | Less (often purpose-specific) | High (any legitimate business expense) |

| Repayment Structure | Fixed monthly payments over a set term | Minimum monthly payments (revolving balance) |

| Credit Building Impact | Reports to business bureaus (varies by lender) | Consistently reports to business bureaus (stronger for early credit building) |

| Collateral Required | Often for larger loans or less established businesses | Rarely (personal guarantee common for startups) |

| Ideal Use Cases | Large investments, expansion, acquisitions, equipment | Daily expenses, cash flow management, marketing, small purchases |

| Impact on Personal Credit | Can be significant (especially for startups) | Can be significant (personal guarantee common) |

| Access to Funds | One-time disbursement of full amount | Continuous access up to limit as balance is repaid |

| Common Fees | Origination, closing, prepayment penalties | Annual fees, late fees, foreign transaction fees |

—

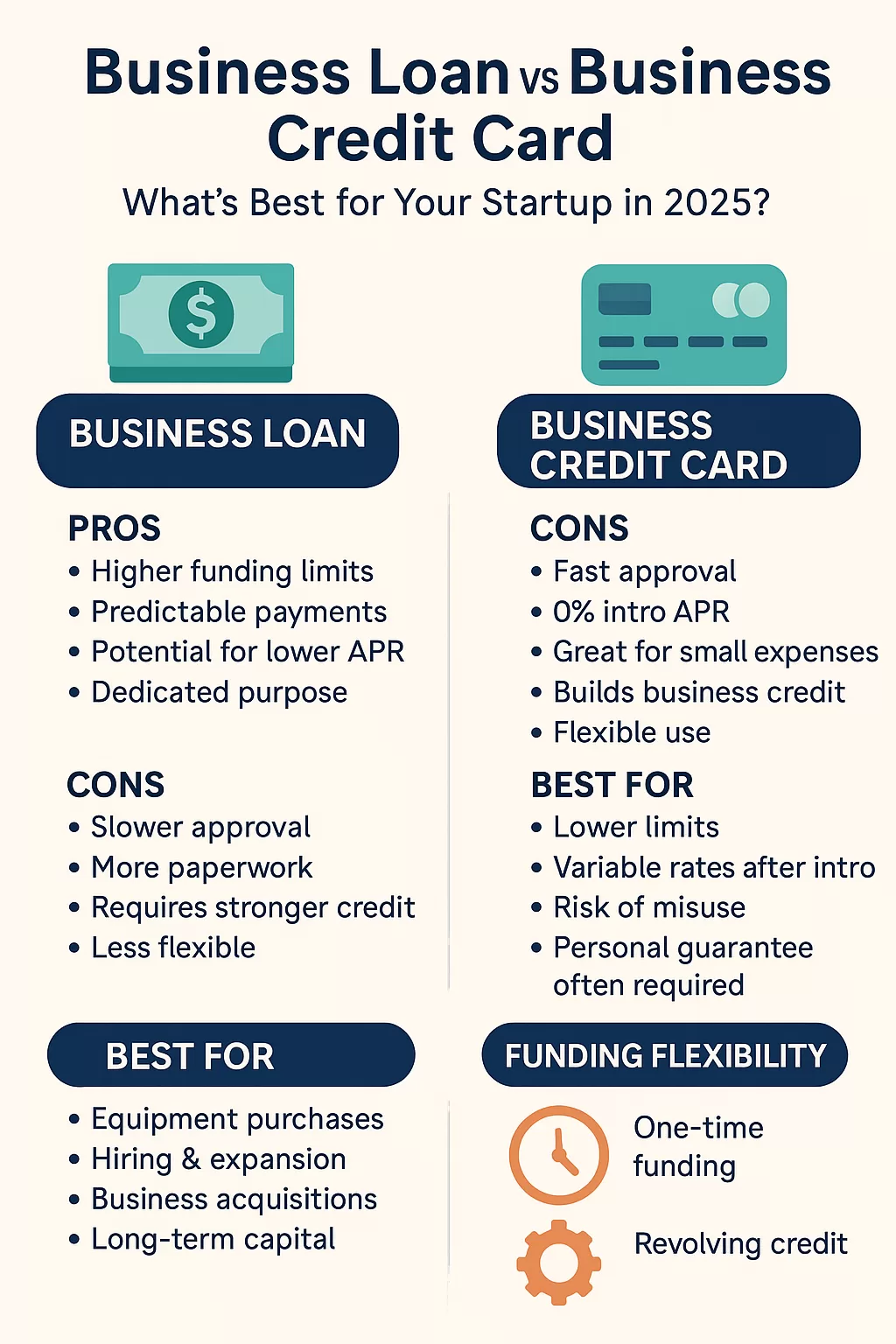

5. Pros & Cons: An Exhaustive Breakdown of Each Funding Tool

Understanding the distinct advantages and disadvantages of business loans and credit cards is crucial for making an informed decision. This section provides an exhaustive breakdown, highlighting their strengths and weaknesses for startup founders.

Business Loan — Pros and Cons

Pros:

- Higher Funding Limits: Business loans typically offer significantly larger amounts of capital compared to credit cards, making them suitable for substantial investments such as purchasing commercial real estate, acquiring heavy machinery, or funding large-scale research and development projects.

- Predictable Payments: With fixed monthly payments over a set term, business loans provide stability and predictability, which is crucial for long-term financial planning and budgeting. This allows founders to forecast cash flow with greater accuracy.

- Potential for Lower APR: For well-qualified businesses, especially those with established credit histories or collateral, loan interest rates can be considerably lower than the variable APRs of business credit cards, particularly after an introductory period.

- Dedicated Purpose: Loans are often approved for specific, larger projects, which can enforce financial discipline and ensure that capital is allocated as intended for growth initiatives.

- Longer Repayment Terms: Loans can offer extended repayment periods, which spreads out the financial burden and can improve a business’s monthly cash flow by reducing the size of individual payments.

Cons:

- Slower Approval & More Paperwork: The application and approval process for business loans can be lengthy, ranging from weeks to several months, particularly for traditional bank or SBA loans. This involves extensive documentation, financial statements, and sometimes collateral assessments, creating a significant administrative burden.

- Requires Stronger Credit & Business History: Many lenders impose stringent requirements for time in business and minimum annual revenue, along with robust personal credit score and business credit scores, making them harder for very new or pre-revenue startups to obtain.

- Less Flexible: Once funds are disbursed, a business generally cannot easily access more capital without undergoing a new application process, which can be a drawback for dynamic, evolving needs.

- Collateral Risk: For secured loans, pledging assets as collateral means those assets are at risk if the business defaults on its payments.

- Prepayment Penalties: Some business loans include clauses that penalize early repayment, which can negate potential interest savings if a business becomes able to pay off its debt ahead of schedule.

Business Credit Card — Pros and Cons

Pros:

- Fast Approval & Access to Funds: Many business credit card applications are approved within days, sometimes instantly, with virtual cards available for immediate use. This speed is invaluable for urgent needs or seizing time-sensitive opportunities.

- 0% Intro APR: This feature is a significant advantage, allowing businesses to make purchases and repay them without incurring interest for an extended introductory period. This can be a game-changer for managing cash flow and investing in growth without immediate interest costs.

- Great for Recurring Small Expenses: Business credit cards are ideal for day-to-day operational costs, software subscriptions, office supplies, and flexible spending, providing a convenient and efficient way to manage ongoing expenditures.

- Builds Business Credit: Regular and responsible use, including on-time payments and low utilization, helps establish and strengthen a business’s credit profile, separate from the owner’s personal credit. This is crucial for future funding opportunities. (Source: Bankrate).

- Flexible Use: Funds accessed via a business credit card can generally be used for almost any legitimate business expense, offering broad utility without specific purpose restrictions.

- Rewards & Perks: The cashback, travel points, and other benefits offered by many business credit cards can provide tangible value, effectively reducing overall business costs.

Cons:

- Lower Limits: Credit limits on business credit cards are typically much smaller than loan amounts, limiting their utility for large, one-time capital projects or major investments.

- High Variable Rates After Intro: While the 0% intro APR is attractive, the Annual Percentage Rate can jump significantly after this period, making carrying a balance extremely expensive and potentially leading to accumulating high-interest debt.

- Risk of Misuse or Overspending: The easy access to funds can lead to accumulating high-interest debt if not managed carefully, potentially spiraling out of control if spending exceeds repayment capacity.

- Personal Guarantee Often Required: Many business credit cards, especially for startups, require a personal guarantee from the business owner, meaning personal assets could be at risk if the business defaults on its payments.

- Annual Fees: Some premium business credit cards come with annual fees, which can erode the value of rewards if not offset by sufficient spending or benefits.

Both business loans and credit cards can serve as powerful leverage tools for growth or, if mismanaged, can become dangerous debt traps. For credit cards, the 0% introductory APR period represents a significant lever, enabling strategic investments without immediate interest burden. However, carrying a balance beyond this period quickly transforms it into a trap due to the high, variable interest rates that can rapidly inflate the total cost of borrowing. Similarly, for business loans, the fixed payments offer a stable framework for financial planning and major investments, acting as a leverage point. Yet, if the business fails to generate sufficient revenue to consistently cover these predictable payments, the loan can become a trap, potentially leading to default and the loss of pledged collateral. The critical distinction lies in the founder’s financial discipline and the business’s underlying profitability and cash flow management. Therefore, founders must not only understand the inherent features of each financial instrument but also critically assess their own capacity for managing debt and the anticipated return on investment from the funds acquired. This shifts the focus from merely debating “which is better” to a more profound question of “how can this tool be used wisely and sustainably to propel my business forward?”

—

6. Strategic Application: When to Leverage Each Funding Option

The decision between a business loan and a business credit card is not always clear-cut. The optimal choice often depends on the specific financial need, the stage of the startup, and the desired repayment structure. Understanding the strategic application of each tool can significantly impact a business’s financial health and growth trajectory. (Source: NerdWallet).

When to Strategically Use a Business Loan

A business loan is the superior choice when a startup has a clear, substantial need for a lump sum of money that will be repaid over an extended period. These funds are typically earmarked for foundational growth or major milestones that require significant capital injection.

- Major Capital Investments: This includes purchasing commercial real estate, acquiring heavy machinery, or investing in a fleet of vehicles. Loans provide the large sums necessary for these long-term assets.

- Significant Expansion: Funding the opening of new branches, expanding into new geographical markets, or constructing new facilities often necessitates the substantial capital that only a business loan can provide.

- Acquisitions: Purchasing another business or its assets to expand market share or capabilities typically requires a large, structured financing solution.

- Large-Scale Hiring Initiatives: Covering the initial payroll, onboarding costs, and training for a substantial team expansion, particularly when revenue generation from these new hires will take time, is well-suited for a loan. (For efficient payroll management, Gusto offers a fantastic solution.) You might also consider a payroll loan with no tax returns if traditional options are difficult.

- Long-Term Working Capital: For businesses with predictable but lengthy sales cycles, such as manufacturing with long production times or large project-based services, a loan can provide the significant amount of cash needed to bridge lengthy revenue gaps or invest in inventory that will take time to sell.

- Refinancing High-Interest Debt: Consolidating multiple existing business debts, especially those with high interest rates, into a single, lower-rate business loan can significantly reduce monthly payments and overall interest costs.

Need Significant Capital? Explore Loan Options:

For U.S. businesses needing fast access to working capital, National Funding offers loans from $10K to $500K. If you’re an early-stage founder with good personal credit seeking unsecured funding, FundWise Capital specializes in helping you access up to $150K quickly. And for a unique approach to securing 0% interest business credit lines, explore Fund&Grow.

Explore National Funding Loans

Apply for Startup Funding with FundWise

Learn About 0% Business Credit with Fund&Grow

—

When to Strategically Use a Business Credit Card

A business credit card excels in its flexibility, speed, and utility for managing ongoing operational costs. It is the preferred tool for smaller, recurring, or unexpected expenses that require quick access to funds.

- Day-to-Day Operational Expenses: This includes routine purchases like office supplies, utility bills, small equipment, and essential software subscriptions. Tools like Xero for accounting and Bench for bookkeeping are examples of recurring expenses perfectly suited for a business credit card. Consider integrating these with your small business bookkeeping and payroll systems.

- Marketing & Advertising Spend: Paying for digital ad campaigns on platforms like Google or social media, or other promotional activities, is an ideal use case due to the often variable and immediate nature of these costs.

- Travel & Entertainment: Covering flights, hotel accommodations, and dining for business trips or client meetings is efficiently managed with a business credit card, often with the added benefit of travel rewards.

- Bridging Short-Term Cash Flow Gaps: When waiting for client payments or managing seasonal fluctuations in revenue, a business credit card can provide the necessary liquidity to cover immediate expenses and maintain operations without disruption. This is part of effective cash flow management.

- Emergency Funds: For unexpected, smaller business needs that require immediate attention, a credit card offers a rapid solution. You might consider a business loan in 24 hours for more significant urgent needs.

- Building Your Business Credit Profile: Consistent, responsible use of a business credit card, characterized by on-time payments and low utilization, is crucial for establishing and strengthening your business credit, which will be advantageous when seeking larger loans in the future. (For a deeper dive, read our guide on How to Build Business Credit with Fundwise & Fund&Grow).

Secure Your Business Credit Card Today:

For premium solutions to manage expenses and build business credit, explore Amex Business Cards. They often offer competitive 0% intro APRs, robust rewards, and powerful spending features that make them ideal for managing your startup’s day-to-day finances.

—

Case Study Scenarios: Real-World Funding Choices

To illustrate how these financing tools are applied in practical scenarios, let’s examine a few real-world examples that demonstrate effective funding decisions for startups:

- Scenario A: The E-commerce Scale-Up

Need: Alex, founder of a rapidly growing e-commerce store, needs $150,000 to purchase a new, larger inventory batch to meet surging demand and to upgrade warehouse technology for increased efficiency.

Decision & Reasoning: Business Loan. This situation calls for a substantial, one-time capital injection directly tied to tangible assets and inventory that will generate revenue over time. A term loan provides the necessary lump sum with predictable, long-term repayment, aligning with the expected revenue generation cycle of the inventory. Alex successfully secured an online term loan with a 12% APR over 3 years, allowing for stable budgeting. The fixed payments ensured that the capital expenditure was managed without disrupting the daily operational cash flow.

“The loan allowed us to scale our inventory without disrupting daily cash flow. The fixed payments made budgeting straightforward, giving us the confidence to invest big.”

- Scenario B: The SaaS Startup’s Lean Launch

Need: Maya, a new founder of a Software-as-a-Service (SaaS) startup, requires $8,000 for initial software subscriptions (CRM, project management tools), digital marketing tools, and a small ad campaign to acquire early users. She possesses a strong personal credit history but has no business revenue yet.

Decision & Reasoning: Business Credit Card (with 0% Intro APR). For smaller, immediate, and recurring expenses, a business credit card offers quick access to funds and, crucially, a 0% introductory APR period. This allows Maya to defer interest payments while she focuses intensely on achieving product-market fit and generating initial revenue. Furthermore, consistent and responsible use of the card immediately begins building her business credit profile, a vital step for future financing. The speed of approval and the flexibility for various small expenditures made this the ideal choice for a pre-revenue startup.

“The 0% intro APR on my business credit card was a lifesaver. It gave us breathing room to test marketing channels without immediate interest burden, which was critical in our lean launch phase.”

- Scenario C: The Hybrid Growth Strategy (Optimal)

Need: Ben’s consulting firm is profitable and experiencing consistent growth. He needs $75,000 to hire two new senior consultants—a significant, long-term investment in human capital—and simultaneously requires a flexible solution for ongoing client entertainment, travel, and software licenses.

Decision & Reasoning: Both, Strategically Combined. Ben implements a dual-pronged approach. He secures a business line of credit for the hiring initiative, allowing him to draw funds as needed for salaries and onboarding without committing to a large lump sum upfront. Concurrently, he utilizes a premium business credit card for daily operational expenses, client entertainment, and business travel, leveraging its robust rewards program and advanced expense tracking features. This integrated strategy optimizes capital allocation, ensures stable cash flow, and allows the business to benefit from the strengths of both financing tools: fixed, lower-cost capital for major, long-term investments, and flexible, revolving credit for ongoing operational needs and continued credit building.

“Using a line of credit for our team expansion and a credit card for daily operations gives us both stability and agility. It’s the best of both worlds for managing growth effectively.”

—

7. Building Business Credit Faster: Which Tool Propels Your Profile?

Both business loans and business credit cards can contribute significantly to building a strong business credit profile, but they often do so through different mechanisms and with varying degrees of impact, particularly for startups. A robust business credit profile is paramount for future financial accessibility, enabling easier qualification for larger funding amounts and securing more favorable terms, while also establishing the business’s financial independence from the founder’s personal credit. (Source: Forbes).

Business Credit Cards & Reporting

Business credit cards are frequently more direct and consistent reporters to major business credit bureaus, including Dun & Bradstreet, Experian Business, and Equifax Business. This consistent reporting means that every on-time payment and responsible use of the credit line directly contributes to building a positive business credit history. Maintaining low credit utilization (keeping balances well below the credit limit) further enhances the credit score. For a nascent business, this makes credit cards a powerful and accessible instrument for rapidly establishing a positive credit profile from scratch.

For startups, business credit cards often initially rely heavily on the founder’s personal credit score for approval. This reliance serves as a bridge. However, through consistent and responsible use, characterized by on-time payments and prudent management of the credit line, the business itself begins to forge its own independent credit profile. This transition from personal credit dependence to business credit independence is a crucial step in the financial maturation of a startup. It eventually allows the business to secure more substantial funding and better terms without solely leveraging the founder’s personal credit, thereby reducing personal financial risk. Thus, business credit cards are not merely tools for spending; they are strategic instruments for establishing the business’s distinct financial identity and progressively reducing the founder’s personal liability over time.

Business Loans & Reporting

While many business loan lenders also report payment activity to business credit bureaus, the frequency and the specific bureaus to which they report can vary more widely than with credit card issuers. Larger, traditional bank loans, once established, often have a significant positive impact on a business’s credit score due to the substantial amount of credit extended and the long-term repayment history. Some alternative lenders, such as FundWise Capital and National Funding, are also known for their commitment to reporting payment activity, thereby contributing to the credit-building efforts of their borrowers.

Strategic Use for Credit Building

For optimal business credit building, a dual approach is often recommended. Starting with a business credit card can provide early and consistent reporting, laying a strong foundation for your business’s credit history. As the business matures and demonstrates consistent revenue, layering in a business loan for larger, strategic investments will further diversify the credit profile and demonstrate the business’s capacity to manage different types of debt responsibly. For a deeper dive into building your business credit, refer to our comprehensive article: How to Build Business Credit with Fundwise & Fund&Grow.

—

8. Top Lenders & Business Credit Cards for Startups in 2025

Choosing the right financial partner is as critical as selecting the appropriate funding type. This section provides actionable recommendations for lenders and business credit cards that are particularly well-suited for startup founders in 2025, highlighting why each partner can be a valuable asset to a growing business.

Business Loan & Funding Partners:

- National Funding:

Description: Ideal for established businesses (typically requiring 6+ months in operation and at least $250K in annual revenue) that need rapid access to working capital. National Funding offers loans ranging from $10,000 to $500,000 with quick approvals, focusing on providing essential capital for growing businesses to manage cash flow, purchase inventory, or fund expansion initiatives. You can read more about National Funding business loan requirements and rates for 2025.

- FundWise Capital:

Description: Specializes in unsecured funding solutions tailored for early-stage startups. If a founder possesses a decent personal credit score but the business itself has a limited or nascent credit history, FundWise Capital can assist in accessing up to $150,000 quickly without requiring collateral. Their approach often leverages the founder’s personal credit to secure initial business funding, bridging the gap until the business establishes its own robust credit profile.

- Fund&Grow:

Description: A unique membership program designed to help founders strategically leverage their personal credit to acquire substantial 0% interest business credit lines, potentially up to $250,000. This is an excellent option for businesses looking to fund growth without incurring immediate interest payments, effectively converting personal credit strength into significant, interest-free business capital for a defined period. Learn more about business lines of credit with bad credit.

Business Credit Card Partners:

- Amex Business Cards:

Description: American Express offers a robust suite of business credit cards that are highly regarded for startups and small businesses. Their offerings often include competitive 0% introductory APRs, generous rewards programs (such as cashback or travel points that can be highly valuable), and powerful spending features. These cards are ideal for managing daily operational expenses, optimizing cash flow, and actively building a strong business credit profile through consistent, responsible use. (Source: FinanceBuzz).

Essential Business Tools (Supporting the Financial Ecosystem):

While the core comparison revolves around loans and credit cards, successful funding acquisition and management are deeply intertwined with a robust financial infrastructure. Lenders scrutinize organized financials and clear cash flow. Integrating the following tools provides a holistic solution for financial health, making a founder more “fundable” and better equipped to manage any debt.

- Mercury Bank:

Description: A modern banking platform specifically built for startups and tech companies. Mercury offers FDIC-insured accounts, virtual cards for secure online spending, and seamless integrations with popular accounting software. It provides an efficient and streamlined way to manage your business finances, crucial for maintaining clarity and control over your capital. You can find more helpful resources on our About page.

- Bench:

Description: Provides online bookkeeping services and tax support tailored for small businesses. Maintaining accurate and up-to-date financial records is not just good practice; it’s essential for securing future funding, as lenders require clear financial statements. Bench helps ensure your books are always in order, providing peace of mind and readiness for financial review. This complements our guide on small business bookkeeping and payroll.

- Xero:

Description: A leading cloud-based accounting software that simplifies invoicing, expense tracking, and comprehensive financial reporting. Xero is a must-have for modern startups to keep their books organized, automate routine tasks, and generate insights into their financial performance, all of which are vital for effective financial management and demonstrating fiscal responsibility to potential lenders.

A startup’s ability to secure and effectively manage financing is significantly enhanced by having strong financial systems in place. The recommendation of these supporting tools adds substantial value by addressing the underlying readiness required for successful funding acquisition and prudent financial stewardship. (Source: Forbes).

—

9. Optimizing Your Funding Strategy: The Power of Combined Use

The most successful startup founders understand that business loans and business credit cards are not mutually exclusive; rather, they are complementary tools that, when used strategically, can create a robust and flexible financial foundation. This synergistic approach allows a business to leverage the distinct advantages of each instrument to meet diverse capital needs at different stages of growth.

The Synergistic Approach

- Strategic Allocation: Business loans are best reserved for large, long-term, and predictable investments. This includes significant capital expenditures like purchasing equipment, acquiring real estate, or funding major business expansions. These are typically one-time, high-cost initiatives that benefit from the structured repayment and potentially lower interest rates of a loan. You can also explore best business loans for startups in 2025.

- Flexible, Short-Term Needs: Conversely, business credit cards are ideal for flexible, short-term, and revolving needs. This encompasses day-to-day operational expenses, inventory top-ups, marketing campaigns, and managing short-term cash flow fluctuations. Their quick access to funds and revolving nature make them perfect for dynamic and immediate financial requirements.

Building a Strong Financial Foundation

This combined approach allows a startup to build both strong business credit and access significant capital as needed for different growth stages. Starting with a business credit card can provide early and consistent reporting, laying a strong foundation for your business’s credit history. As the business matures and demonstrates consistent revenue, layering in a business loan to fund larger, strategic investments will further diversify the business’s credit profile and demonstrate the business’s capacity to manage various forms of debt.

Avoiding Pitfalls

Utilizing both tools wisely helps avoid common financial pitfalls. It prevents over-reliance on high-interest credit card debt for large, long-term projects, which can quickly become unsustainable. Simultaneously, it mitigates the inflexibility of relying solely on loans for small, recurring, or unexpected operational needs, which can be cumbersome and inefficient to finance through repeated loan applications.

A startup’s funding needs dynamically evolve with its growth stages. In the earliest phases, business credit cards, often initially backed by the founder’s personal credit, are typically the most accessible and effective instruments for building initial business credit and managing lean operations. As the business gains traction, generates consistent revenue, and establishes a more robust operational history, it becomes eligible for more substantial, often lower-interest, business loans. These loans are then strategically deployed for larger capital expenditures or significant growth initiatives that align with the business’s increased maturity. The concept of “optimal combined use” is therefore not a static prescription but a dynamic strategy that requires founders to align the most appropriate funding tool with the business’s current stage of development and its specific capital requirements. This necessitates a forward-looking financial roadmap, where the use of loans and credit cards is adapted as the business expands and its funding needs transform. (Source: Forbes).

—

10. Frequently Asked Questions (FAQ)

What is better for startups: a business loan or a business credit card?

There is no single “better” option; the optimal choice depends entirely on a startup’s specific needs and stage of development. Business credit cards are generally more suitable for immediate, flexible, and smaller expenses, such as daily operational costs, marketing spend, or bridging short-term cash flow gaps. They are also excellent for building initial business credit, especially with the advantage of 0% introductory APRs. In contrast, business loans are typically better suited for larger, one-time investments like purchasing equipment, funding major expansions, or significant hiring initiatives, as they offer larger sums and predictable repayment terms over a longer period. The most effective strategy for many successful startups involves strategically using both tools in tandem to leverage their respective strengths. (Source: NerdWallet).

Can I get a business credit card with no revenue?

Yes, it is often possible for startups to obtain a business credit card even with no or very limited revenue. Many business credit card issuers, particularly when evaluating applications from early-stage businesses, primarily rely on the business owner’s personal credit score for approval. While some lenders may inquire about projected revenue or require a minimum time in business, a strong personal credit history (e.g., a FICO score in the good to excellent range) is usually the most critical factor for pre-revenue or newly established businesses to qualify.

Do business loans help credit?

Yes, generally, business loans contribute positively to a business’s credit profile. Most reputable business loan lenders report payment activity to major business credit bureaus such as Dun & Bradstreet, Experian Business, and Equifax Business. Consistent, on-time payments on a business loan can significantly enhance and improve your business credit score, demonstrating responsible debt management. However, it is important to note that reporting practices can vary by lender, with some smaller or niche lenders potentially not reporting to all bureaus, or with different reporting frequencies. It is always advisable to confirm a lender’s reporting practices before committing to a loan. (Source: Forbes).

What is the average APR for a business loan in 2025?

In 2025, the average Annual Percentage Rate (APR) for business loans varies widely, influenced by factors such as the loan type, the lender, the borrower’s creditworthiness, and the current economic climate. For well-established businesses securing traditional bank term loans, APRs might range from 6% to 15%. However, for online lenders or short-term loans, particularly those catering to startups or businesses with less robust credit, APRs could range from 15% to 30% or even higher, reflecting the perceived risk. Government-backed SBA loans typically offer some of the most competitive rates due to their federal guarantees. (Source: Bankrate).

How quickly can I get funding from a business credit card vs. a loan?

Business credit cards offer significantly faster access to funds compared to most business loans. Applications for business credit cards can often be approved within minutes to a few days, and virtual cards may even be available for immediate use upon approval. In contrast, the timeline for securing a business loan can vary considerably. Some online lenders might offer funding within a few days (e.g., business loan in 24 hours), but traditional bank loans or government-backed SBA loans typically involve a more extensive underwriting process that can take several weeks or even months before funds are disbursed. This difference in speed is a critical consideration for businesses with urgent capital needs. (Source: Ramp).

—

Conclusion: Empower Your Startup’s Financial Future

Understanding the nuances of a business loan vs business credit card is more than just financial literacy; it’s a strategic advantage that empowers startup founders to make informed decisions about their capital. By knowing when and how to deploy each tool, you equip your startup with the agility and financial backing it needs to thrive in the competitive landscape of 2025 and beyond.

While business credit cards offer unparalleled flexibility, speed, and an excellent pathway to building initial business credit, especially with their valuable 0% introductory APR periods, they come with the caveat of potentially high variable interest rates if balances are carried long-term. Conversely, business loans provide larger capital sums, predictable repayment structures, and often lower overall interest costs for major, long-term investments, though they typically involve a more rigorous application process and longer approval times.

The most successful founders recognize that these tools are not mutually exclusive. Instead, they leverage both intelligently. This often means starting with a flexible business credit card for day-to-day operational needs and initial credit building, then strategically layering in a substantial business loan as growth demands larger, more structured investments. This dynamic approach ensures that capital is always aligned with the specific needs and stage of the business, optimizing both immediate cash flow and long-term financial stability. (Source: Forbes).

Explore your best funding options now — whether you want a $100K loan, a 0% credit card, or both!

—