SBA Loan Checklist 2025: Everything You Need to Qualify Faster

Unlock the capital your startup needs with this essential guide to SBA loan qualification.

Table of Contents

- 1. Introduction: Demystifying SBA Loans for Your Startup

- 2. Why SBA Loans Are a Game Changer for Small Businesses

- 3. The Essential SBA Loan Checklist for 2025 Qualification

- 4. Beyond the Checklist: Strategies to Qualify Faster

- 5. Common Pitfalls to Avoid in Your SBA Loan Application

- 6. What If an SBA Loan Isn’t Right for You (Yet)? Explore Alternatives

- 7. Download Your Free Business Loan Approval Checklist

- 8. Additional Resources to Fuel Your Startup’s Growth

- Conclusion: Empower Your Startup’s Financial Future

1. Introduction: Demystifying SBA Loans for Your Startup

For many startups and small businesses, securing capital is the biggest hurdle to growth. While traditional bank loans can be tough to get for newer ventures, and venture capital isn’t for everyone, SBA loans (guaranteed by the U.S. Small Business Administration) offer a lifeline. They come with favorable terms, lower interest rates, and longer repayment periods, making them an attractive option for founders.

However, the application process for an **SBA loan** can be complex, often requiring meticulous preparation and a deep understanding of the requirements. That’s where our SBA Loan Checklist 2025 comes in. This comprehensive guide is designed to simplify the journey, helping you understand everything you need to qualify faster and boost your chances of approval for vital government-backed funding.

Whether you’re looking for working capital, equipment financing, or funds for real estate, knowing the exact **SBA loan requirements** before you apply can save you countless hours and significantly improve your outcome. For a general understanding of different funding types, you might also find our guide on Business Credit vs. Business Loan helpful.

2. Why SBA Loans Are a Game Changer for Small Businesses

SBA loans aren’t direct loans from the government; rather, the SBA guarantees a portion of the loan made by participating lenders (banks, credit unions, and online lenders). This guarantee reduces the risk for lenders, making them more willing to lend to small businesses that might not otherwise qualify for conventional loans.

Key benefits that make SBA loans a preferred choice for startups and growing businesses include:

- Lower Down Payments: Often less than conventional loans.

- Longer Repayment Terms: Reducing monthly payments and improving cash flow.

- Competitive Interest Rates: Capped by the SBA, typically lower than other small business loans.

- Flexible Uses: Can be used for a wide range of business purposes, from working capital to equipment and real estate.

The most common SBA loan programs for small businesses are:

- SBA 7(a) Loans: The most flexible and popular program, offering up to $5 million for various general business purposes, including working capital, equipment, and real estate.

- SBA Microloans: Smaller loans up to $50,000, typically for startups and underserved communities, focused on working capital or inventory.

- SBA 504 Loans: Designed for major fixed-asset purchases like real estate or machinery, typically up to $5 million (with no maximum project size).

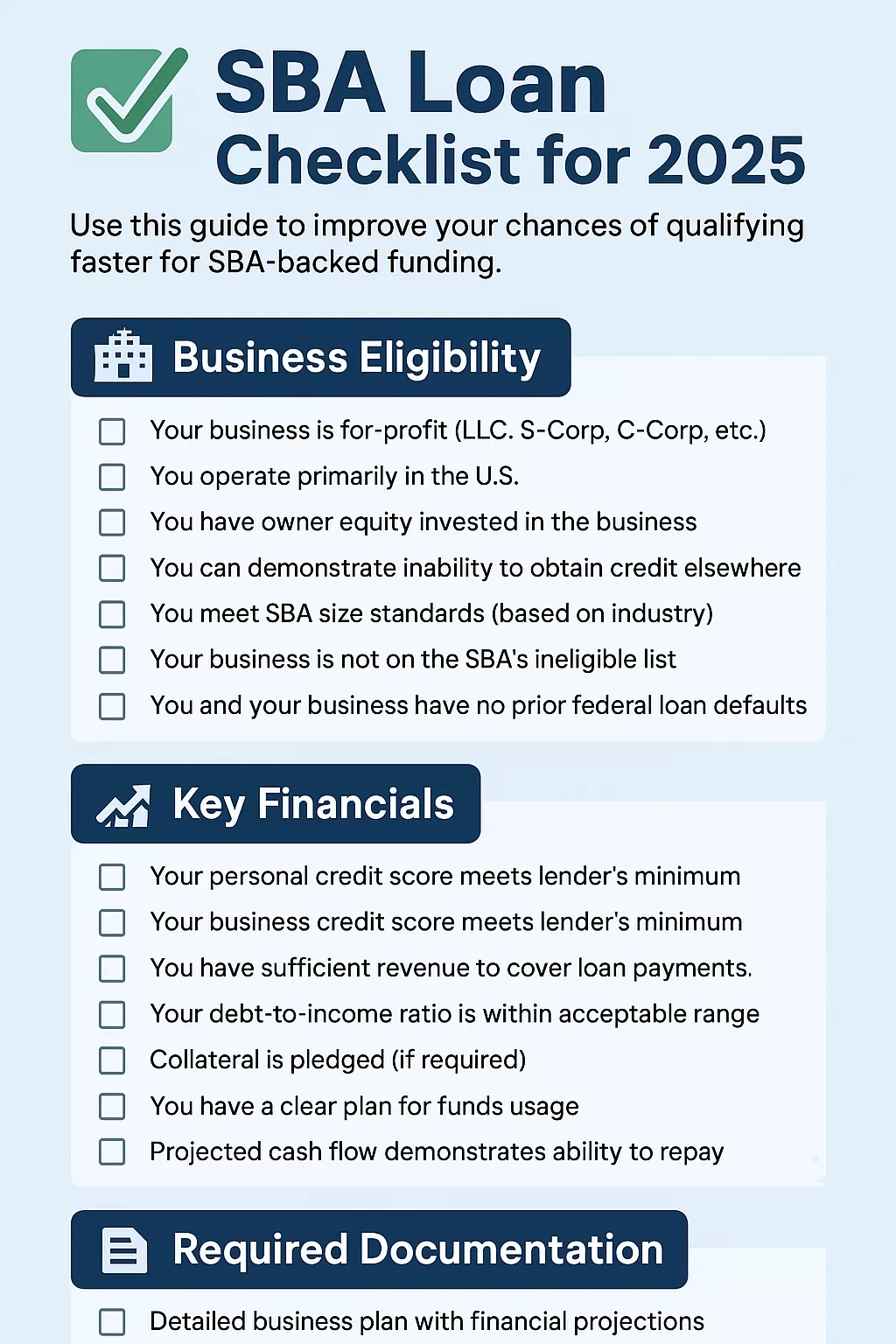

3. The Essential SBA Loan Checklist for 2025 Qualification

To give your **SBA loan application** the best chance of success, thorough preparation is key. Here’s your detailed **SBA loan checklist** for 2025, broken down into critical categories:

Business Eligibility & Requirements

Key Financial Qualifications

Boost Your Business & Personal Credit: If your credit needs a lift to qualify for SBA or other small business administration loans, consider working with experts. FundWise Capital and Fund&Grow specialize in helping founders build strong business credit profiles, which is essential for any future lending. Learn more in our guide on How to Build Business Credit with Fundwise & Fund&Grow.

✅ Apply for Startup Funding with FundWise

🚀 Learn About 0% Business Credit with Fund&Grow

Required Documentation

Gathering all necessary paperwork is perhaps the most time-consuming part of the **SBA loan application**. Be prepared with these documents:

- Profit & Loss (P&L) Statements: For the last three years (if applicable) and a current interim statement.

- Balance Sheets: For the last three years (if applicable) and a current interim statement.

- Cash Flow Statements: Showing how money moves in and out of your business.

- Pro Forma Financials: Detailed projections for new businesses or significant expansions.

- Business Tax Returns: For the last three years.

- Personal Tax Returns: For the last three years for all owners.

- Articles of Incorporation/Organization.

- Business licenses and permits.

- Fictitious name registration (DBA), if applicable.

- Business lease agreement (if applicable).

- Franchise agreements (if applicable).

- Personal background (résumés for all owners/key management).

- Ownership percentages of all partners.

- SBA Forms (e.g., SBA Form 1919 – Borrower Information Form).

4. Beyond the Checklist: Strategies to Qualify Faster

Having the items on your **SBA loan checklist** is one thing; presenting them in a way that speeds up approval is another. Here’s how to streamline your qualification process:

- Meticulous Financial Preparation: Ensure all financial statements are accurate, up-to-date, and organized. Discrepancies or missing information will cause delays. Consider professional accounting services like Bench.co to keep your books impeccable.

- Proactively Boost Your Credit Scores: If your personal or business credit scores are borderline, take steps to improve them before applying. Pay down debt, resolve collection accounts, and ensure consistent on-time payments. Remember, a strong credit profile is key for any type of business financing.

- Craft a Compelling Business Plan: A well-written plan demonstrates your understanding of the market, your strategy, and your ability to execute. It should clearly articulate how the loan funds will be used and repaid.

- Choose the Right Lender: Not all SBA-approved lenders are created equal. Some specialize in certain loan types or industries, or have faster processing times. For a broader look at funding options, explore our guides on the Best Startup Loans for 2025 and Fastest Loans for Startups.

- Seek Professional Guidance: Working with an experienced loan broker or business consultant can significantly increase your chances of approval by ensuring your application is complete and compelling.

5. Common Pitfalls to Avoid in Your SBA Loan Application

Even with a thorough **SBA loan checklist**, many applicants fall prey to common mistakes that lead to delays or outright rejections. Avoid these pitfalls:

- Incomplete or Inaccurate Applications: The most frequent reason for delays. Double-check every field, every document.

- Poor Credit History: A weak personal or business credit score is a major red flag for lenders. This highlights why building strong business credit is so vital.

- Insufficient Collateral or Equity: While not always a deal-breaker, insufficient assets can raise concerns, especially for larger loans.

- Lack of a Clear Business Plan or Use of Funds: Lenders need to understand your vision and how their money will be used responsibly.

- Not Addressing Past Financial Issues: Don’t hide past bankruptcies or defaults; explain them honestly and what you’ve done to mitigate future risks.

- Underestimating Time & Effort: The SBA loan process requires patience and persistence. Rushing or expecting instant approval will lead to frustration.

6. What If an SBA Loan Isn’t Right for You (Yet)? Explore Alternatives

While an SBA loan offers great terms, it’s not the only funding path, and it might not be the fastest or easiest for every startup, especially those that are very new or have specific needs. For a detailed comparison of options, check out our article on Business Loan vs Business Credit Card. Don’t get discouraged if you don’t qualify immediately for an SBA loan or need capital quicker than an SBA loan can provide.

Explore Diverse Funding Solutions:

National Funding: Offers fast and flexible business loans, often with less stringent requirements than traditional banks or SBA. Great for businesses needing working capital quickly.

→ Explore National Funding for Faster Loans

FundWise Capital & Fund&Grow: These partners are invaluable for startups looking to build their business credit or access unsecured funding based on personal credit. They can help you get the capital you need now, or strengthen your profile for future SBA applications.

✅ Apply for Startup Funding with FundWise

🚀 Learn About 0% Business Credit with Fund&Grow

Amex Business Cards: For flexible spending, managing cash flow, and building a separate business credit history, a business credit card can be a powerful tool. Many offer 0% intro APR periods, making them an excellent choice for immediate, smaller needs. See the latest Amex Offers here.

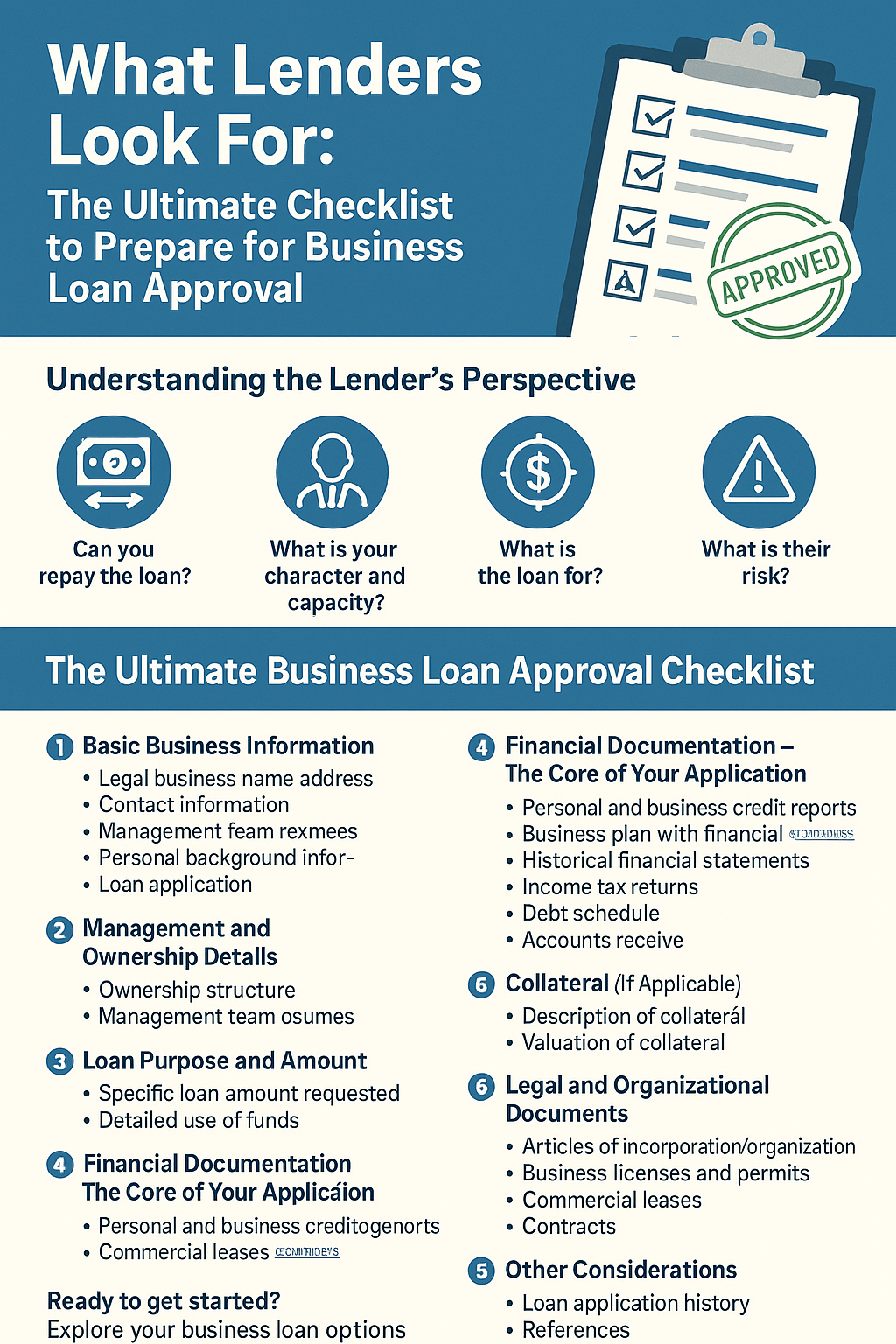

7. Download Your Free Business Loan Approval Checklist (Lead Magnet)

To further empower your funding journey, we’ve created a comprehensive, printable version of our “Business Loan Approval Checklist.” This downloadable resource condenses key requirements and preparation steps, making it an invaluable tool for any entrepreneur seeking capital.

It’s the perfect companion to this SBA-specific guide, helping you organize your documents and understand the broader lending landscape. Download it today and take the first step towards securing your business’s future!

8. Additional Resources to Fuel Your Startup’s Growth

Continue to build your financial expertise with these valuable guides from Incorporate & Grow:

- Business Credit vs. Business Loan: Which One Fuels Growth? – Understand the fundamental differences in how these financial instruments work.

- Best Startup Loans for 2025 – A broader overview of various loan options available to new businesses.

- Fastest Loans for Startups – Discover options when you need capital on an accelerated timeline.

- Amex Offer Page – Explore exclusive business credit card offers.

- How to Build Business Credit with Fundwise & Fund&Grow – A deep dive into strategies for establishing and improving your business credit score.

Conclusion: Empower Your Startup’s Financial Future

Navigating the intricacies of an SBA loan can feel daunting, but with this SBA loan checklist, you’re well-equipped to approach the application process with confidence in 2025. Preparation is your strongest asset, ensuring you meet all **SBA loan requirements** and present your business in the best possible light.

Remember, if an SBA loan isn’t the right fit right now, or if you need to strengthen your profile, there are numerous other viable **startup business loan options** and partners ready to help you secure the capital necessary for your growth. The key is to be informed and proactive.

Ready to secure your business funding? Download our comprehensive checklist and explore top loan options today!

⬇️ Download Your Free Checklist!

→ Explore Loan Options